More like 'easing off the brakes than stepping on the gas'

Article content

It seems Canada’s largest bank isn’t expecting a whole lot of upside in the short-term from what appears to be the start of a campaign by the Bank of Canada to bring interest rates down.

Interest rate cuts won’t provide an immediate boost to Canada’s lagging economy or the debt payment relief some households are seeking, a new analysis from Royal Bank of Canada suggests.

Advertisement 2

Article content

Despite signs around the world that economies are starting to rally, including in the euro area and the United Kingdom, Canada’s economy has continued to struggle on a GDP-per-capita basis with the metric running three per cent below levels seen in 2019. Craig Wright, senior vice-president and chief economist at Royal Bank of Canada, notes that is a 10 per cent swing relative to the U.S., where per capita GDP is up seven per cent in that timeframe.

“The global economic growth backdrop has shown signs of improvement, but Canada’s economy continues to underperform,” Wright said in a report published on Wednesday. “The Bank of Canada’s pivot to cut interest rates in June is more akin to easing off the monetary policy brakes than stepping on the gas.”

Indebted households will obviously cheer rate cuts, but “the lagged impact of past interest rate increases will continue to push debt payments higher,” Wright said, estimating that moves by the central bank likely won’t lead to an uptick in growth until sometime next year. For 2024, RBC predicts real GDP will come in at one per cent rising to 1.8 per cent in 2025.

Posthaste

Article content

Advertisement 3

Article content

For the first time in four years, the Bank of Canada cut its benchmark lending rate by 25 basis points to 4.75 per cent on June 6, citing, among its reason for doing so, a weakening economy, excess supply and slowing inflation.

“We assume another 75 basis points of BoC cuts this year, but that will still leave the level of interest rates above those neutral levels and subtract on net from economic growth, just by less than currently,” Wright said.

The reason for that is the expected cuts would still leave the bank’s rate well above the 2.25 per cent to 3.25 per cent range that the Bank of Canada considers neutral, meaning it neither stimulates nor suppresses economic growth.

Looking at the mortgage landscape, Royal Bank’s chief economist estimates there are approximately $200 billion worth of mortgages, most with four- and five-year terms, that will be renegotiated this year with $275 billion up for renewal in 2025.

Households will feel the impact of higher rates, but Wright said the jump in payments appears “manageable” against the increases in incomes that have risen dramatically from pre-pandemic levels.

Advertisement 4

Article content

“The expected payment shock this year will still be large for individual households impacted, but accounts for a relatively small 0.2 per cent of total Canadian household incomes, according to our estimates,” Wright said.

However, the bank’s chief economist doesn’t foresee rate cuts helping with housing affordability due to a “structural” shortage of accomodation, nor does he see lower rates helping with declining productivity.

RBC also produced GDP forecasts for the provinces.

Ontario, Quebec and British Columbia are expected to grow the slowest — 0.5 per cent, 0.7 per cent and 0.8 per cent, respectively — of the provinces given that they are home to many of Canada’s most indebted households.

GDP in the Prairie provinces is expected to expand more than the country as a whole with Alberta’s economy growing 1.7 per cent as “households and businesses — which took past interest rate hikes in stride — have already amped up spending activity in anticipation of rate cuts,” Wright said.

“A slight pickup in oil prices should help as well.”

Correction: RBC is calling for a total of four interest rate cuts in 2024, not five as an earlier version of the headline stated.

Advertisement 5

Article content

Sign up here to get Posthaste delivered straight to your inbox.

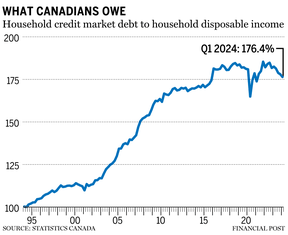

Statistics Canada says the amount Canadians owe relative to their income in the first quarter edged lower compared with the fourth quarter of 2023 as growth in household disposable income outpaced the growth in debt.

The agency says household credit-market debt as a proportion of household disposable income was 176.4 per cent in the first three months of the year on a seasonally adjusted basis.

The result compared with 178.0 per cent in the fourth quarter of 2023.

In other words, there was $1.76 in credit-market debt for every dollar of household disposable income in the first quarter of 2024.

Meanwhile, the household debt-service ratio, measured as total obligated payments of principal and interest on credit market debt as a proportion of household disposable income, was 14.91 per cent in the first quarter of 2024 compared with 14.98 per cent in the fourth quarter of 2023.

The move came as household disposable income rose 1.9 per cent, while debt payments increased 1.4 per cent. — The Canadian Press

Advertisement 6

Article content

- Today’s Data: Canada manufacturing and wholesale sales for April

- Earnings: Kroger

Recommended from Editorial

Problems arise when the generative language AI chatbots — such as OpenAI OpCo LLC’s ChatGPT, Microsoft Corp.’s Copilot, or Meta Platforms Inc.’s AI — deliver what looks like sound financial advice, but it’s either incorrect, incomplete or not in someone’s best interests.

If you aren’t familiar enough with the topic to discern what helps from what hurts, the answers can steer you in the wrong direction. With that in mind, here are three ways advice from AI tools can help solve or deepen your money woes

FP Answers

Are you worried about having enough for retirement? Do you need to adjust your portfolio? Are you wondering how to make ends meet? Drop us a line at aholloway@postmedia.com with your contact info and the general gist of your problem and we’ll try to find some experts to help you out while writing a Family Finance story about it (we’ll keep your name out of it, of course). If you have a simpler question, the crack team at FP Answers led by Julie Cazzin or one of our columnists can give it a shot.

Advertisement 7

Article content

McLister on mortgages

Want to learn more about mortgages? Mortgage strategist Robert McLister’s Financial Post column can help navigate the complex sector, from the latest trends to financing opportunities you won’t want to miss. Read them here

Today’s Posthaste was written by Gigi Suhanic, with additional reporting from Financial Post staff, The Canadian Press and Bloomberg.

Have a story idea, pitch, embargoed report, or a suggestion for this newsletter? Email us at posthaste@postmedia.com.

Bookmark our website and support our journalism: Don’t miss the business news you need to know — add financialpost.com to your bookmarks and sign up for our newsletters here.

Article content

Posthaste: 4 interest rate cuts expected this year likely won't boost Canadian economy, RBC says - Financial Post

Read More

Comments