Toronto's financial district on Feb. 27, 2012.Nathan Denette/The Canadian Press

John Rapley is a political economist at the University of Cambridge and managing director of Seaford Macro.

If you wake up in the morning with a punishing cold, will you a) call in sick to work and take the day to restore yourself or b) medicate the symptoms away and force yourself to keep going? Most of us, given the choice, would take the first option.

Yet when it comes to recessions, we keep going for door b). Over the past 30 years, economic policy in Western countries has been substantially shaped by the New Keynesian school of economics, which came up with a novel prescription for recessions: stimulate demand by cutting interest rates, after which, if need be, the government can pump some money into the economy via such means as bank bailouts, tax cuts or stimulus cheques.

On the face of it, this method’s record of success speaks for itself. Recessions across the West have steadily become rarer, shorter and shallower. Meanwhile depressions, which were a regular and devastating feature of earlier capitalism, have pretty much disappeared. Needless to say, economists feel triumphant. They’ve been medicating away the pain of recessions, but not treating the chronic condition causing it.

Over the past decade, for instance, it’s become painfully evident that Westerners are growing increasingly unhappy. In the period since the 2008 crash, an opiate crisis tore the U.S. apart, other countries saw mental-health epidemics (particularly among young people), street protests rose, politics grew increasingly divided as populists urged their supporters to violence and public support for democracy cratered.

It’s not that difficult to detect a link between this rising discontent and the state of the economy – even Donald Trump worked it out. The way governments intervened and stimulated their economies directly resulted in an economic model that has inflated profits and asset-values while depressing real wages, which effectively transferred income from workers to owners.

And when, in the past couple years, workers finally started clawing back some of their losses with better wage packages, central bankers told them to stop being greedy. No wonder folks are angry. This anger has been fermenting for the past 30 years and lies at the heart of many of our social problems.

Most central bankers, and the economists advising them, will retort that it isn’t their concern, that their job is merely to keep inflation low and economies growing and that, at least before the pandemic, they were doing just that.

Yet this sounds a bit like grading your own homework. If a doctor has prescribed you painkillers for a cold and it develops into a kidney infection, you’d hardly take well to his declaration of success since the cold was now gone. Even if we allowed their claim that economists aren’t responsible for actually making people happy, it’s still not clear that the conventional method of overcoming recessions is working on its own terms.

Although recessions have got weaker, so too have the subsequent recoveries. Part of the difficulty is that by pumping money indiscriminately into the economy, central banks have kept ‘zombie firms’ alive and thereby prevented new, more dynamic ones getting off the ground. So too, as we’ve seen in Canada, have they inflated real estate bubbles, which suck investment away from productive uses and make it hard to start new businesses.

It’s as if central bankers reckon that, like a 1970s English soccer coach with an injured player, their sole job is to get the economy back on its feet quickly so it can ‘run off’ the injury. Yet, while the economy is moving again, it’s clearly limping.

Meanwhile there’s a hidden price to this approach. Faced with the rising costs of an aging population and a less productive work force, governments have kept their deficits relatively contained mostly by reducing the state’s wealth. By letting infrastructure run down, privatizing national firms and selling off government properties, governments have effectively sold the family jewels to pay the bills. Over the past decade, most Western governments have seen their net wealth diminish, which could crimp their ability to meet future obligations.

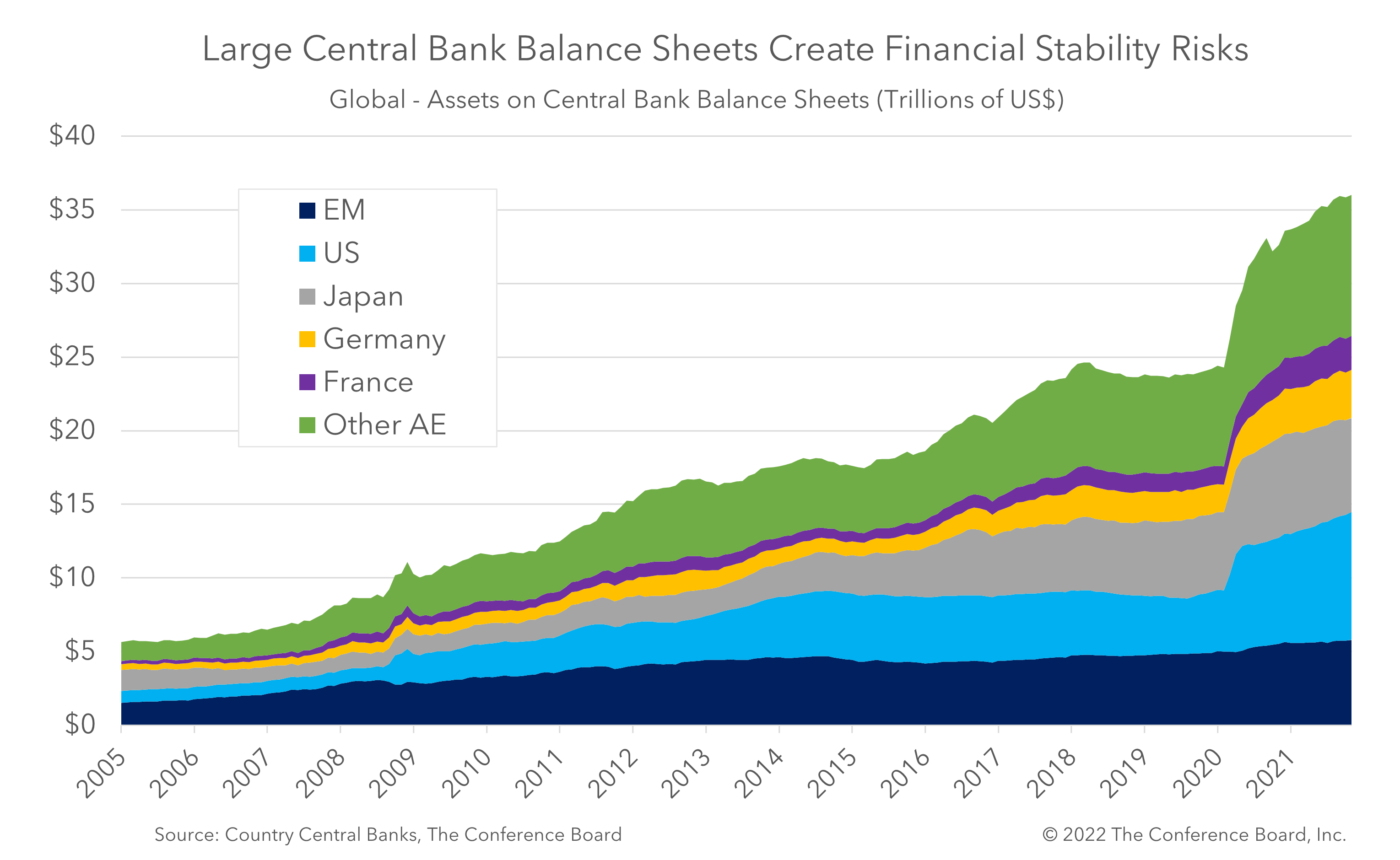

Meanwhile central banks have bloated their balance sheets, leaving them with what amounts to huge overdrafts. It’s as if they’ve treated a chronic condition with painkillers: Now that the effects have worn off and tolerance has built, treatment requires ever bigger doses. Sooner or later an addiction builds, while the underlying conditions worsens. There are obvious limits to this strategy.

As central banks struggle to make effective policy amid stubborn inflation and governments battle to ward off recessions, those limits are arguably approaching. The next time a recession comes around, we should do things differently. We should diagnose the underlying condition and come up with a proper rehab program. Because like the colleague who keeps coming to work sick, the economy is working, but its health keeps deteriorating.

Opinion: How trying to fix recessions and economic decline actually creates more problems - The Globe and Mail

Read More

:format(jpeg)/cloudfront-us-east-1.images.arcpublishing.com/tgam/7UE3RXRDKJKOVCZ6WC5GFNDHLU.JPG){kind=link}

{kind=link}

No comments:

Post a Comment