OTTAWA — Economic growth resumed in January and came in better than first expected following a small contraction in December, Statistics Canada said Friday.

Real gross domestic product rose 0.5 per cent to start the year, the agency said, beating its initial estimate for a gain of 0.3 per cent for the month and reversing a contraction of 0.1 per cent in the final month of 2022.

Statistics Canada also said its initial estimate for February indicates growth continued with a gain of 0.3 per cent, though it cautioned the figure will be updated.

"There were many indications that the economy got off to a solid start in 2023, but today's double-barrelled blast of strength is well above even the most optimistic views," BMO chief economist Douglas Porter wrote in a report.

"Even if growth stalls in March, it now looks like Q1 will post growth of 2.5 per cent, up from a flat read in Q4. While we continue to look for a notable cooldown in the next two quarters, we are bumping up our GDP growth estimate for all of 2023 by three ticks to 1.0 per cent."

The growth in January came as goods-producing industries gained 0.4 per cent for the month, while services-producing industries rose 0.6 per cent.

Statistics Canada said many of the main drivers for growth in January also contributed the most to the decline in December.

The wholesale trade, transportation and warehousing, and mining, quarrying and oil and gas extraction sectors all rebounded after falling in the previous month.

Wholesale trade gained 1.8 per cent in January, helped by wholesalers of machinery, equipment and supplies, while the mining, quarrying and oil and gas extraction sector grew 1.1 per cent after falling 3.3 per cent in December.

The transportation and warehousing sector added 1.9 per cent in January, more than offsetting a drop of 1.1 per cent in December that was due in part to bad weather.

This report by The Canadian Press was first published March 31, 2023.

A construction worker prepares a recently poured concrete foundation, in Boston, on March 17.Michael Dwyer/The Associated Press

The U.S. economy maintained its resilience from October through December despite rising interest rates, growing at a 2.6 per cent annual pace, the government said Thursday in a slight downgrade from its previous estimate. But consumer spending, which drives most of the economy’s growth, was revised sharply down.

The government had previously estimated that the economy expanded at a 2.7 per cent annual rate last quarter.

The rise in the gross domestic product – the economy’s total output of goods and services – for the October-December quarter was down from the 3.2 per cent growth rate from July through September. For all of 2022, the U.S. economy expanded 2.1 per cent, down significantly from a robust 5.9 per cent in 2021.

The report suggested that the economy was losing momentum at the end of 2022.

Consumer spending rose at a 1 per cent annual rate last quarter, downgraded from a 1.4 per cent increase in the government’s previous estimate. It was the weakest quarterly gain in consumer spending since COVID-19 slammed the economy in the spring of 2020. Spending on physical goods, like appliances and furniture, which had initially surged as the economy rebounded from the pandemic recession, fell for a fourth straight quarter.

More than half of last quarter’s growth came from businesses restocking their inventories, not an indication of underlying economic strength.

Most economists say they think growth is slowing sharply in the current January-March quarter, in part because the Federal Reserve has steadily raised interest rates in its drive to curb inflation.

The resulting surge in borrowing costs has walloped the housing industry and made it more expensive for consumers and businesses to spend and invest in major purchases. As a consequence, the economy is widely expected to slide into a recession later this year.

The central bank has raised its benchmark interest rate nine times over the past year. The Fed’s policy-makers are betting that they can stick a so-called soft landing – slowing growth just enough to tame inflation without tipping the world’s biggest economy into recession.

Yet as higher loan costs spread through the economy, analysts are generally skeptical that the United States can avoid a downturn. The main point of debate is whether a recession will prove mild, with only minor damage to hiring and growth, or severe, with waves of layoffs.

The financial conditions that led to the collapse of Silicon Valley Bank on March 10 and Signature Bank two days later – the second– and third-biggest bank failures in U.S. history – are also expected to slow the economy. Banks are likely to impose stricter conditions on loans, which help fuel economic growth, to conserve cash to meet withdrawals from jittery depositors.

“The economy ended 2022 with marginally less momentum,” Oren Klachkin and Ryan Sweet of Oxford Economics wrote in a research note. “Looking ahead, the economy will face the full brunt of tighter credit conditions and Fed policy this year, and inflation is set to stay above its historical trend.” They added: “We expect a recession to hit in the second half of 2023.”

In the meantime, the job market remains robust and has exerted upward pressure on wages, which feed into inflation. The pace of hiring is still healthy, and the unemployment rate is near a half-century low. The confidence and spending of consumers remain relatively solid.

Thursday’s report from the Commerce Department was its third and final estimate of GDP for the fourth quarter of 2022. On April 27, the department will issue its initial estimate of growth in the current first quarter. Forecasters surveyed by the data firm FactSet have estimated that growth in the January-March quarter is decelerating to a 1.4 per cent annual rate.

OTTAWA — Economic growth resumed in January and came in better than first expected following a small contraction in December, Statistics Canada said Friday.

Real gross domestic product rose 0.5 per cent to start the year, the agency said, beating its initial estimate for a gain of 0.3 per cent for the month and reversing a contraction of 0.1 per cent in the final month of 2022.

Statistics Canada also said its initial estimate for February indicates growth continued with a gain of 0.3 per cent, though it cautioned the figure will be updated.

"There were many indications that the economy got off to a solid start in 2023, but today's double-barrelled blast of strength is well above even the most optimistic views," BMO chief economist Douglas Porter wrote in a report.

"Even if growth stalls in March, it now looks like Q1 will post growth of 2.5 per cent, up from a flat read in Q4. While we continue to look for a notable cooldown in the next two quarters, we are bumping up our GDP growth estimate for all of 2023 by three ticks to 1.0 per cent."

The growth in January came as goods-producing industries gained 0.4 per cent for the month, while services-producing industries rose 0.6 per cent.

Statistics Canada said many of the main drivers for growth in January also contributed the most to the decline in December.

The wholesale trade, transportation and warehousing, and mining, quarrying and oil and gas extraction sectors all rebounded after falling in the previous month.

Wholesale trade gained 1.8 per cent in January, helped by wholesalers of machinery, equipment and supplies, while the mining, quarrying and oil and gas extraction sector grew 1.1 per cent after falling 3.3 per cent in December.

The transportation and warehousing sector added 1.9 per cent in January, more than offsetting a drop of 1.1 per cent in December that was due in part to bad weather.

This report by The Canadian Press was first published March 31, 2023.

This section was produced by the editorial department. The client was not given the opportunity to put restrictions on the content or review it prior to publication.

Economy's resilience means higher interest rates remain a possibility this year

Get the latest from Kevin Carmichael straight to your inbox

A welder works in British Columbia. Gross domestic product, as measured by industrial output, increased 0.5 per cent in January from the previous month.Photo by Abigail Saxton/Bloomberg

Article content

Statistics Canada on March 31 said Canada’s economy surged back to life at the start of the year after stalling at the end of 2022, complicating the Bank of Canada‘s efforts to get inflation back to its two-per-cent target. Here’s what you need to know:

Advertisement 2

THIS CONTENT IS RESERVED FOR SUBSCRIBERS ONLY

Subscribe now to read the latest news in your city and across Canada.

Unlimited online access to articles from across Canada with one account

Get exclusive access to the National Post ePaper, an electronic replica of the print edition that you can share, download and comment on

Enjoy insights and behind-the-scenes analysis from our award-winning journalists

Support local journalists and the next generation of journalists

Daily puzzles including the New York Times Crossword

SUBSCRIBE TO UNLOCK MORE ARTICLES

Subscribe now to read the latest news in your city and across Canada.

Unlimited online access to articles from across Canada with one account

Get exclusive access to the National Post ePaper, an electronic replica of the print edition that you can share, download and comment on

Enjoy insights and behind-the-scenes analysis from our award-winning journalists

Support local journalists and the next generation of journalists

Daily puzzles including the New York Times Crossword

REGISTER TO UNLOCK MORE ARTICLES

Create an account or sign in to continue with your reading experience.

Access articles from across Canada with one account

Share your thoughts and join the conversation in the comments

Enjoy additional articles per month

Get email updates from your favourite authors

Article content

Gross domestic product, as measured by industrial output, increased 0.5 per cent in January from the previous month, more than reversing a 0.1 per cent drop in December.

GDP increased an additional 0.3 per cent in February, according to Statistics Canada’s “flash estimate,” which is based on preliminary data.

Seventeen of the 20 broad industries that Statistics Canada monitors posted gains, led by wholesaling, which increased 1.8 per cent from December. Mining, quarrying, and oil and gas gained 1.1 per cent.

The Canadian dollar increased somewhat, and short-term bond yields rose, as traders repositioned amid expectations that the Bank of Canada will leave interest rates high for long

Article content

Article content

Backstory

Canada’s economy was supposed to be in a recession by now. At least that was the vibe for much of last year, as economists reckoned the most severe burst of inflation in four decades and the most aggressive series of rate hikes in the Bank of Canada’s history would combine to sink the recovery from the COVID-19 crisis.

Article content

Advertisement 3

Article content

The economy slowed, but nowhere near as much as forecasters predicted, as a surprisingly strong labour market offset the effects of higher living costs. Earlier this year, it looked like Canada’s impressive run had finally run out of track when Statistics Canada reported that GDP growth stalled in the fourth quarter, aligning with the Bank of Canada’s prediction that there would be essentially no growth for the first part of 2023.

But some economists observed the fourth-quarter numbers were influenced by an unusually large depletion of inventories, suggesting the economy might still have some spark. That appears to be the case, as many industries that posted declines in December rallied in January.

Where is the growth coming from?

Advertisement 4

Article content

The latest GDP numbers suggest the rebound from December was a mix of predictable reversions to trend and a surprisingly resilient current of demand.

Recall that Enbridge Inc. spent time in December cleaning up a spill from its Keystone pipeline in Kansas, which slowed oil exports to the United States. Shipments had resumed to normal in January. Another example of one-off explanations: output by wholesalers of machinery and equipment surged 2.4 per cent in January as suppliers received a batch of imports destined for the massive LNG Canada liquefied natural gas project in British Columbia.

But math doesn’t explain everything.

The jobless rate is near a historic low, which appears to be offsetting higher inflation and debt-servicing costs. Wages are growing faster than prices for the first time in two years, bolstering consumer confidence. Retail trade, accommodation and food services, and arts and entertainment — industries that are closely linked to consumer discretionary spending — all posted solid gains. The demand destruction that so many economists predicted hasn’t happened yet.

Advertisement 5

Article content

What does it mean for interest rates?

The Bank of Canada stopped raising interest rates for the first time in a year on March 8. Headline inflation had been steadily dropping from its peak in June, so policymakers said it was appropriate to pause and assess the situation. Governor Tiff Macklem had made it clear he didn’t want to cause a recession if he could avoid it.

However, policymakers emphasized they were still worried about inflation and would err on the side of getting year-over-year increases in the consumer price index back to two per cent. (Inflation was 5.2 per cent in February.) That means another interest rate increase will be on the table when Macklem and his deputies gather to update policy on April 12.

Advertisement 6

Article content

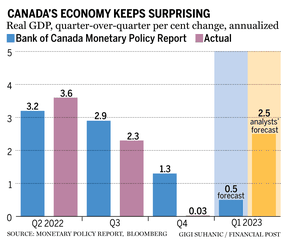

Faster economic growth will be a concern for the central bank only because it will exert upward pressure on inflation. (That’s why it tends to take a recession to bring price increases under control.) But policymakers will probably look at these numbers and call it a wash. Their quarterly economic outlook in January predicted a 1.3 per cent annual rate of growth in the fourth quarter, not zero, which is what Statistics Canada’s actual tally produced.

The Bank of Canada’s outlook for growth in the first quarter was 0.5 per cent, and some economists said the January and February monthly figures imply the economy is growing at an annual rate of about 2.5 per cent.

The gains in January and February could represent some of those sparks of strength the Bank of Canada already thought it was seeing. That calculation will probably be enough to leave interest rates unchanged in April. But the economy’s resilience means higher interest rates remain a possibility this year, and the rate cuts that some forecasters see on the horizon remain a distant bell.

An earlier version of this story stated that the Bank of Canada predicted the economy grew at an annual rate of 0.5 per cent in the fourth quarter. That was its prediction for the first quarter. The mistake has been corrected.

Share this article in your social network

Comments

Postmedia is committed to maintaining a lively but civil forum for discussion and encourage all readers to share their views on our articles. Comments may take up to an hour for moderation before appearing on the site. We ask you to keep your comments relevant and respectful. We have enabled email notifications—you will now receive an email if you receive a reply to your comment, there is an update to a comment thread you follow or if a user you follow comments. Visit our Community Guidelines for more information and details on how to adjust your email settings.

(Bloomberg) -- China’s biggest state-owned banks delivered profit gains last year after boosting lending to help cushion the economy from a slowdown triggered by the nation’s strict pursuit of Covid zero.

Industrial & Commercial Bank of China Ltd., the country’s biggest lender by assets, reported Thursday that net income rose 3.5% to 360.5 billion yuan ($52.4 billion), short of analysts’ estimates. Other banks topped or met forecasts, including Agricultural Bank of China Ltd., whose profit rose 7.4% to 259 billion yuan last year. Bank of China Ltd. posted a 5% profit increase, while Bank of Communications Co. earlier reported a 5.2% gain.

China’s $54 trillion banking industry has been pushing to extend more credit in the past year as it grappled with low demand. A strict Covid-zero policy, abandoned in late 2022, had weighed on economic growth and sapped consumer confidence. A persistent slump in the property market has also impacted business.

Analysts have been cautious about the outlook for banks, even after several of the big banks reported profits that beat estimates. Although China’s economic activity is rebounding this year after lifting Covid restrictions — with banks extending a record amount of new loans in January — headwinds still exist.

China’s push for state lenders to lower borrowing cost for small businesses and home buyers, coupled with a potential loan prime rate cut this year, could pressure margins in 2023, Bloomberg Intelligence analyst Francis Chan said in a note Thursday. Most of the big banks reported declines in net interest margins last year.

Here is a summary of the banks’ full-year net income, net interest margins and non-performing loan ratios from a year earlier:

During your trial you will have complete digital access to FT.com with everything in both of our Standard Digital and Premium Digital packages.

Standard Digital includes access to a wealth of global news, analysis and expert opinion. Premium Digital includes access to our premier business column, Lex, as well as 15 curated newsletters covering key business themes with original, in-depth reporting. For a full comparison of Standard and Premium Digital, click here.

Change the plan you will roll onto at any time during your trial by visiting the “Settings & Account” section.

What happens at the end of my trial?

If you do nothing, you will be auto-enrolled in our premium digital monthly subscription plan and retain complete access for 65 € per month.

For cost savings, you can change your plan at any time online in the “Settings & Account” section. If you’d like to retain your premium access and save 20%, you can opt to pay annually at the end of the trial.

You may also opt to downgrade to Standard Digital, a robust journalistic offering that fulfils many user’s needs. Compare Standard and Premium Digital here.

Any changes made can be done at any time and will become effective at the end of the trial period, allowing you to retain full access for 4 weeks, even if you downgrade or cancel.

When can I cancel?

You may change or cancel your subscription or trial at any time online. Simply log into Settings & Account and select "Cancel" on the right-hand side.

You can still enjoy your subscription until the end of your current billing period.

What forms of payment can I use?

We support credit card, debit card and PayPal payments.

French economists and public auditors alike breathed a sigh of relief as the national statistics agency INSEE on Tuesday published an annual report showing that the country’s 2022 budget deficit dipped below 5% of GDP. Public debt also slightly decreased. Despite these hopeful figures, France still remains one of the most-indebted countries in the EU.

Pointing to France’s better-than-expected post-pandemic economic performance – thanks to which GDP showed an increase of 2.6% year-on-year in 2022 – Finance Minister Bruno Le Maire congratulated the French economy on bringing the budget deficit down to 4.7%. The government had previously set the target to 5% of GDP.

French public debt has likewise benefitted from the recovering economy. “The resilience of our economy has allowed us to reduce public debt to 111.6% of GDP and reach our target in public finances”, Le Maire said on Tuesday while underlining his “determination” to rebalance the books.

In order to do so, the French finance minister has vowed to cut back on public spending by several billion euros.

“Public spending currently amounts to 57% of national output... I would like to bring this number down to 54% by 2027, close to the European average of 52%”, Le Maire told Franceinfoover two weeks ago.

Growing public debt

It's a seemingly difficult undertaking, as the government has spent massively over the past couple of years in an effort to prop up an economy weakened by faltering business during the Covid-19 pandemic and galloping inflation spurred by the ongoing war in Ukraine.

“Between 2020 and 2023, €300 billion have been injected into the economy”, deputy director of SciencePo University's centre for economic research (OFCE) Mathieu Plane told Le Mondeas he pointed to discretionary expenditures decided by the government.

On top of spending on vaccination campaigns and other sanitary measures during the pandemic, the government has passed several stimulus plans since last year to avoid a looming recession, which include energy bill vouchers, price caps and early revaluations of social benefits to shelter the French population from rising costs of living.

In addition to previously approved tax cuts, state guaranteed loans and funding of unemployment benefits under President Emmanuel Macron’s 2020 “whatever it takes” slogan, the government has granted subsidies to energy-intensive companies to shield them from increasing production costs.

While France has narrowly avoided a recession by putting the brakes on inflation, estimated at 5.4% for this year by the Bank of France, public debt has as a result risen from 97.4% of GDP in 2019 to 111.6% or €2.95 trillion in 2022.

Ranking in the EU

The figure for public debt might appear shocking at first glance, especially when set against EU fiscal rules outlined in the 1997 Stability and Growth Pact, which stipulate that national debt should not surpass 60% of GDP.

Budget deficit, meanwhile, should not surpass 3% according to the same guidelines.

Although France has clearly exceeded EU limits, it is far from alone among its European partners in the euro zone.

Greece remains the EU member with the highest ratio of 178.2% of government debt to GDP by the end of the third quarter of 2022, the latest data published by Eurostat shows.

Next comes Italy, with a debt to GDP ratio of 147.3%.

Portugal comes third at 120.1%, while Spain is fourth at 115.6% followed by France at 113.4%.

The average national debt to GDP ratio in the euro zone stands at 93%.

Despite a current suspension of EU fiscal rules until 2024 due to heightening economic uncertainty, French financial institutions remain concerned about the high debt ratio.

“French public debt is not sustainable”, former rapporteur at France’s Court of Auditors and FIPECO association President François Escalle said in a March analysis, pointing to decades of accumulating debt and an increasingly volatile market.

Governor of the Bank of France François Villeroy de Galhau called for the government to reduce public debt to below 100% of GDP a few months ago as he warned against rising interest rates.

The European Central Bank (EBC) on March 16 increased interest rate by 50 base points to 3.5%, the sixth consecutive hike since July 2022.

Meanwhile, French 10-year bonds currently yield around 2.8% after surpassing 3% earlier this year.

“The annual cost of public debt is the second item on the State budget” right after public spending on education, Montaigne Institute economy and State action director Lisa Thomas-Darbois told AFP.

Compounded by the fact that one tenth of French public debt is indexed to inflation, public debt interest has cost France around “35€ billion in 2021 and around 50€ in 2022”, Ecalle said.

Ecalle also noted limitations on the rescue operations by the European Central Bank (ECB) which has intervened several times in the past to bail out debt-ridden countries such as Greece and Italy, but may not continue to do so for fear of further adding to the financial burden of other EU members.

The ECB may always be willing to bail out countries such as France, Italy and Spain because they are “too big to fail”, but the ultimate risk is the withdrawal of another EU member unwilling to shoulder the financial burden, he said, adding this might lead to further fractures in the union over the long haul.

All the fuss today is about machine learning and ChatGPT. The algorithms associated with them work well if the future is similar to the past. But what if we are at an inflection point in economic and political conditions and the future is different from the past? Will record profit margins, inflated asset prices and low inflation and interest rates of the past 30 years be an accurate reflection of the future? Is this time different?

Maybe we’re already there. Things do not seem to make sense anymore. Have you noticed that economic indicators seem to have stopped working as well and as predictably as they have in the past?

Here are some examples of the puzzling behaviour of economic statistics of recent months.

An inverted yield curve has historically been a good indicator of recessions. For several months now the yield curve has been inverted and yet the U.S. economy has been adding millions of jobs, leading to an historic low unemployment rate. Employment is booming while the economy at large is not.

Consumer sentiment, as reflected in the University of Michigan surveys, and consumer spending have tended historically to move together. But this time around, while consumer sentiment took a nosedive, consumer spending and credit card balances keep growing, reaching record highs.

Construction employment and homebuilder stocks are rising while housing permits and housing starts are falling. Normally, homebuilder stock prices would reflect the collective wisdom of financial markets about housing activity. Not this time.

Bond markets are expecting inflation to recede to the Fed’s target rate of 2 per cent. In this case, the real interest rate, implicit in the 10-year treasuries yield of between 3.5-4 per cent, is 1.5-2 per cent, which is close to historical averages. But prior to the Silicon Valley Bank debacle, some surveys pegged expected inflation to about 3 per cent going forward. Assuming the real rate is the same, this implied a 10-year treasuries yield of between 4.5-5 per cent. Either the bond market was out of line or forecasters’ inflation models do not work as well as in the past.

And oil prices are around US$70 a barrel despite the recent banking crisis and at a time when the economy is slowing down and believed to be entering a recession. Based on past experience at this point in the business cycle oil prices should be at US$50 or less. But they are not. Which begs the question: What will happen to oil prices when the economy enters a growth phase, especially with the opening of China after the COVID-19 lockups?

And the list of puzzling contradictions goes on. Having said that, someone may argue that the labour statistics, for example, are a lagging indicator and show where the economy was, not where it is going. While this is true, the magnitude of divergence between labour statistics and economic activity is so much higher than they’ve been historically. That makes one wonder what is going on.

It could be that many of these puzzling statistics are the result of “survey fatigue,” as Bloomberg Businessweek calls it. The publication reports that there has been a decline in response rates for many surveys government agencies use to collect economic data.

For example, employer response to the Current Employment Statistics survey, according to the publication, which collects payroll and wage data each month, has declined to under 45 per cent by September, 2022, from about 60 per cent at the end of 2019. The issue here is the non-response bias: that people who are not responding to the survey are systematically different from those who do, and this skews results. Could weakening trust in institutions and governments be behind the decline in response rates in recent years? If this is the case, the problem is serious and difficult to reverse or eliminate.

As a result, machine learning algorithms that need massive and good quality data about the past and assume that the future will look pretty much like the past may not work. Then what? Should we re-examine our old models? Or will human intervention always be required? Machine learning will not be able to replace investor insight and “between the lines” reading of nuanced economic numbers.

George Athanassakos is a professor of finance and holds the Ben Graham Chair in Value Investing at the Ivey Business School, University of Western Ontario.

Be smart with your money. Get the latest investing insights delivered right to your inbox three times a week, with the Globe Investor newsletter.Sign up today.

A year of surging prices and rising interest rates has put fresh stress on Canadian households struggling to make ends meet.

Landmark investments in the green transition from the United States have turned up the heat on the Canadian government as it looks to stay competitive with the economic juggernaut south of the border.

And after years of higher spending and a surging recovery from the COVID-19 pandemic, storm clouds are gathering in the economy, putting new scrutiny on government coffers.

Can Ottawa thread the needle through the competing pressures and economic uncertainty while still meeting Canadians’ ends?

Here’s what economists think.

Budget planning in a 'challenging time'

The federal budget comes at a “challenging time” for Freeland and Prime Minister Justin Trudeau, says Sahir Khan, vice-president at the University of Ottawa’s Institute of Fiscal Studies and Democracy.

Now in their third term of governing, Khan tells Global News that the Liberals’ second budget of their current mandate is set to arrive amid a “change in context.”

He says the Liberals have had the “good fortune” of inheriting large revenue surprises in previous budgets, which has helped the government spend more while staying fiscally sustainable.

But government revenues are set to dry up with the economy slowing, Khan warns, even as spending priorities mount.

Among the pressures facing the government are commitments already made on a new health-care accord with the provinces, defence spending both at home and in Ukraine and the green energy transition.

Freeland gives detailed outline of funding in proposed health-care plan

“Storm clouds” are gathering for a possible recession on the horizon, Khan notes, and the federal government will feel pressure to “keep some of their powder dry” for emergency spending to resuscitate the economy if the worst-case scenarios come to pass.

Randall Bartlett, senior director of Canadian economics at Desjardins, says that even with the first quarter of the year off to a stronger start than most economists anticipated, the government still finds itself in a bind with uncertainty about how much the economy slows this year.

“It’s a challenging environment to do budget planning overall,” he tells Global News.

How will inflation impact the budget?

A surging economy through the COVID-19 recovery helped push government revenues higher and Ottawa spent much of this money on support for Canadians hit hard by the pandemic.

While those programs have largely wound up, a recent analysis from the Bank of Montreal showed that government spending per capita is still 11.3 per cent higher than in the pre-pandemic era.

Bartlett says that while government revenues generally see a boost amid high inflationary periods, the federal government is about to experience the “insidious” nature of rising price pressures on the downturn.

Canada’s inflation rate cools to 5.2%

Government spending supports that are indexed to inflation, such as Old Age Security (OAS), are now costing more, just as subsiding inflation and a cooling economy are set to slow government revenue growth, he says.

“We’re going to continue to see those knock-on effects of high inflation on the spending side, even as those tailwinds to revenues start to fade,” Bartlett says.

But Bartlett adds that the government is facing “a lot of political pressure” to continue to spend to support vulnerable households.

Some economists worry that too much direct financial support from the federal government will end up fuelling inflation, as Canadians use their contributions to buy more goods and services and end up stimulating the economy all over again.

More on Canada

Top officials at the Bank of Canada, which has raised its benchmark interest rate aggressively over the past year to cool the economy and tame inflation, have said that letting up on pandemic-era stimulus sooner could have limited inflation.

In order to avoid driving inflation higher with government support, Ottawa will need to be “well-targeted” in its spending plans, says Lindsay Tedds, associate professor of economics at the University of Calgary.

Rather than sweeping tax cuts, which would lessen the burden on households but could inadvertently spur more spending, Tedds tells Global News that the Liberals could again double the GST credit or top up guaranteed income supplements.

More students turning to food banks as inflation shrinks already tight budgets

Doing it this way would ensure government spending goes more towards Canadians who need it to make ends meet on the basic necessities, she says.

“We’re talking about just trying to get them through being able to pay rent and buy groceries and things like that. So it doesn’t have an inflationary impact,” she says.

Khan says the government could also “stagger” its promises, with spending ramping up in years three, four and five of its budget horizon. Doing so could allow the Liberals to keep money back to respond to emergencies while also showing Canadians they’re listening to affordability concerns, he says.

Pressure from the U.S. demands action

Economists who spoke to Global News say the federal government is feeling pressure to respond to the U.S.’s Inflation Reduction Act, which rolled out a number of incentives for companies to make investments in the green economy south of the border.

Despite restrictions on the government coffers, the Liberals will need to put a “down payment” on some of the clean energy priorities it has talked about for years, Khan says.

If Ottawa does not roll out its own incentives to compete with the U.S., Canada risks losing jobs and investment from large-scale companies in the green economy, he argues.

“They will suck that capital and those jobs out if we don’t look like we’re doing the same for our industry,” Khan says of the U.S.

“There’s going to have to be something actually quite tangible in this budget. It can’t just all be narrative.”

Tedds agrees and notes that announcements on measures like carbon capture and storage will be attractive in Alberta.

Ottawa can’t necessarily go toe-to-toe with American capital, however, and Bartlett says the government should focus spending on industries where Canada has a “comparative advantage.”

He highlights critical minerals as one such area where Canada could position itself in the green economy.

‘Champagne taste’ and a ‘beer bottle budget’

Tedds says Canadians should “moderate their expectations” for the upcoming budget.

While it’s possible Canada avoids the worst of the economic downturn, the outlook is “too unpredictable” for the Liberal government to offer significant relief or big-ticket items in this budget, she says.

Tedds notes she’d like to see an overhaul of the employment insurance program to ensure that when and if Canada’s jobless rate starts to rise, the government is ready to support Canadians through the downturn.

“We really should be recession-ready. There are some sectors that are really hurting, tech being one of them. We’ve seen massive layoffs, especially here in Calgary. And so there are people hurting,” she says.

Despite all the pressures facing the Liberals in their third term in office, Khan says the Trudeau government will need to demonstrate that it’s still “got some fire in its belly” and can deliver results for Canadians.

“I think this time it’s going to be less about aspiration and more about perspiration,” he says.

As opposed to a newly elected government delivering a budget of change in its first spending plans, the Liberals will have to prove they still have ideas and can make progress on projects that matter to Canadians, Khan says.

He expects the Liberals will devote a fair bit of the budget text to the already announced health-care spending announced in February as a “victory lap” of sorts.

If the government wants to hit every spending priority while maintaining the federal debt-to-GDP ratio — a key fiscal guardrail watched not only by the government but by credit rating agencies and international observers — it may have to find new sources of funding.

Canadian banks are stable, but ‘something is going to break’ in economy: experts

Bartlett says that with the revenue sources drying up and the Liberals under pressure to maintain their fiscal guardrails, tax hikes could be on the table, likely aimed at corporations or higher-income earners.

Otherwise, he says the Liberals might have “champagne tastes,” but they’re working with a “beer bottle budget.”

“They’re not going to get everything on their wish list,” he says. “And so they need to they need to be mindful of that and exercise some genuine prudence.”

A year of surging prices and rising interest rates has put fresh stress on Canadian households struggling to make ends meet.

Landmark investments in the green transition from the United States have turned up the heat on the Canadian government as it looks to stay competitive with the economic juggernaut south of the border.

And after years of higher spending and a surging recovery from the COVID-19 pandemic, storm clouds are gathering in the economy, putting new scrutiny on government coffers.

Can Ottawa thread the needle through the competing pressures and economic uncertainty while still meeting Canadians’ ends?

Here’s what economists think.

Budget planning in a 'challenging time'

The federal budget comes at a “challenging time” for Freeland and Prime Minister Justin Trudeau, says Sahir Khan, vice-president at the University of Ottawa’s Institute of Fiscal Studies and Democracy.

Now in their third term of governing, Khan tells Global News that the Liberals’ second budget of their current mandate is set to arrive amid a “change in context.”

He says the Liberals have had the “good fortune” of inheriting large revenue surprises in previous budgets, which has helped the government spend more while staying fiscally sustainable.

But government revenues are set to dry up with the economy slowing, Khan warns, even as spending priorities mount.

Among the pressures facing the government are commitments already made on a new health-care accord with the provinces, defence spending both at home and in Ukraine and the green energy transition.

Freeland gives detailed outline of funding in proposed health-care plan

“Storm clouds” are gathering for a possible recession on the horizon, Khan notes, and the federal government will feel pressure to “keep some of their powder dry” for emergency spending to resuscitate the economy if the worst-case scenarios come to pass.

Randall Bartlett, senior director of Canadian economics at Desjardins, says that even with the first quarter of the year off to a stronger start than most economists anticipated, the government still finds itself in a bind with uncertainty about how much the economy slows this year.

“It’s a challenging environment to do budget planning overall,” he tells Global News.

How will inflation impact the budget?

A surging economy through the COVID-19 recovery helped push government revenues higher and Ottawa spent much of this money on support for Canadians hit hard by the pandemic.

While those programs have largely wound up, a recent analysis from the Bank of Montreal showed that government spending per capita is still 11.3 per cent higher than in the pre-pandemic era.

Bartlett says that while government revenues generally see a boost amid high inflationary periods, the federal government is about to experience the “insidious” nature of rising price pressures on the downturn.

Canada’s inflation rate cools to 5.2%

Government spending supports that are indexed to inflation, such as Old Age Security (OAS), are now costing more, just as subsiding inflation and a cooling economy are set to slow government revenue growth, he says.

“We’re going to continue to see those knock-on effects of high inflation on the spending side, even as those tailwinds to revenues start to fade,” Bartlett says.

But Bartlett adds that the government is facing “a lot of political pressure” to continue to spend to support vulnerable households.

Some economists worry that too much direct financial support from the federal government will end up fuelling inflation, as Canadians use their contributions to buy more goods and services and end up stimulating the economy all over again.

More on Canada

Top officials at the Bank of Canada, which has raised its benchmark interest rate aggressively over the past year to cool the economy and tame inflation, have said that letting up on pandemic-era stimulus sooner could have limited inflation.

In order to avoid driving inflation higher with government support, Ottawa will need to be “well-targeted” in its spending plans, says Lindsay Tedds, associate professor of economics at the University of Calgary.

Rather than sweeping tax cuts, which would lessen the burden on households but could inadvertently spur more spending, Tedds tells Global News that the Liberals could again double the GST credit or top up guaranteed income supplements.

More students turning to food banks as inflation shrinks already tight budgets

Doing it this way would ensure government spending goes more towards Canadians who need it to make ends meet on the basic necessities, she says.

“We’re talking about just trying to get them through being able to pay rent and buy groceries and things like that. So it doesn’t have an inflationary impact,” she says.

Khan says the government could also “stagger” its promises, with spending ramping up in years three, four and five of its budget horizon. Doing so could allow the Liberals to keep money back to respond to emergencies while also showing Canadians they’re listening to affordability concerns, he says.

Pressure from the U.S. demands action

Economists who spoke to Global News say the federal government is feeling pressure to respond to the U.S.’s Inflation Reduction Act, which rolled out a number of incentives for companies to make investments in the green economy south of the border.

Despite restrictions on the government coffers, the Liberals will need to put a “down payment” on some of the clean energy priorities it has talked about for years, Khan says.

If Ottawa does not roll out its own incentives to compete with the U.S., Canada risks losing jobs and investment from large-scale companies in the green economy, he argues.

“They will suck that capital and those jobs out if we don’t look like we’re doing the same for our industry,” Khan says of the U.S.

“There’s going to have to be something actually quite tangible in this budget. It can’t just all be narrative.”

Tedds agrees and notes that announcements on measures like carbon capture and storage will be attractive in Alberta.

Ottawa can’t necessarily go toe-to-toe with American capital, however, and Bartlett says the government should focus spending on industries where Canada has a “comparative advantage.”

He highlights critical minerals as one such area where Canada could position itself in the green economy.

‘Champagne taste’ and a ‘beer bottle budget’

Tedds says Canadians should “moderate their expectations” for the upcoming budget.

While it’s possible Canada avoids the worst of the economic downturn, the outlook is “too unpredictable” for the Liberal government to offer significant relief or big-ticket items in this budget, she says.

Tedds notes she’d like to see an overhaul of the employment insurance program to ensure that when and if Canada’s jobless rate starts to rise, the government is ready to support Canadians through the downturn.

“We really should be recession-ready. There are some sectors that are really hurting, tech being one of them. We’ve seen massive layoffs, especially here in Calgary. And so there are people hurting,” she says.

Despite all the pressures facing the Liberals in their third term in office, Khan says the Trudeau government will need to demonstrate that it’s still “got some fire in its belly” and can deliver results for Canadians.

“I think this time it’s going to be less about aspiration and more about perspiration,” he says.

As opposed to a newly elected government delivering a budget of change in its first spending plans, the Liberals will have to prove they still have ideas and can make progress on projects that matter to Canadians, Khan says.

He expects the Liberals will devote a fair bit of the budget text to the already announced health-care spending announced in February as a “victory lap” of sorts.

If the government wants to hit every spending priority while maintaining the federal debt-to-GDP ratio — a key fiscal guardrail watched not only by the government but by credit rating agencies and international observers — it may have to find new sources of funding.

Canadian banks are stable, but ‘something is going to break’ in economy: experts

Bartlett says that with the revenue sources drying up and the Liberals under pressure to maintain their fiscal guardrails, tax hikes could be on the table, likely aimed at corporations or higher-income earners.

Otherwise, he says the Liberals might have “champagne tastes,” but they’re working with a “beer bottle budget.”

“They’re not going to get everything on their wish list,” he says. “And so they need to they need to be mindful of that and exercise some genuine prudence.”

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/tgam/SKR2CE3XWFJEVPDDOCPYWM7XM4.jpg)

/cloudfront-us-east-1.images.arcpublishing.com/tgam/EOAQBER6SZIYBL4UAXX6OXTLPE.JPG)

Comments

Postmedia is committed to maintaining a lively but civil forum for discussion and encourage all readers to share their views on our articles. Comments may take up to an hour for moderation before appearing on the site. We ask you to keep your comments relevant and respectful. We have enabled email notifications—you will now receive an email if you receive a reply to your comment, there is an update to a comment thread you follow or if a user you follow comments. Visit our Community Guidelines for more information and details on how to adjust your email settings.

Join the Conversation