World Economic Forum articles may be republished in accordance with the Creative Commons Attribution-NonCommercial-NoDerivatives 4.0 International Public License, and in accordance with our Terms of Use.

The views expressed in this article are those of the author alone and not the World Economic Forum.

Asia’s fourth-largest economy sees industrial output shrink a worse-than-expected 1.8 percent in August.

South Korea’s factory production fell for a second straight month in August, a warning sign for the global economy as it faces risks from the war in Ukraine to rising interest rates.

Asia’s fourth-largest economy saw industrial output shrink a worse-than-expected 1.8 percent on a seasonally-adjusted monthly basis after falling 1.3 percent in July, government figures showed on Friday.

Compared with the same month a year earlier, factory output rose 1.0 percent, the slowest pace since September 2021.

However, output for the services sector rose 1.5 percent on the month, while retail sales jumped 4.3 percent, the fastest gain since May 2020.

The figures follow a raft of data showing slowing factory output in other major Asian economies, including China, Japan and Taiwan.

China’s factory activity slowed further in September following a decline the previous month, as Beijing’s ultra-strict “zero COVID” policies hit production and sales, according to a private sector survey released on Friday.

South Korea, one of the world’s biggest manufacturers of cars, chips and ships, is seen as a barometer of the health of global trade as its companies span a vast swathe of the world economy.

South Korea’s exports, which account for nearly 40 percent of gross domestic product (GDP), are expected to slow sharply in September, with a survey of economists by the Reuters news agency predicting the slowest growth in nearly two years ahead of the release of official figures next month.

“This is certainly concerning for the domestic and global economy,” Min Joo Kang, senior economist for South Korea and Japan at ING, told Al Jazeera.

“The weaker than expected industrial production was driven by Korea’s main export items such as semiconductors and petrochemicals. This would have a negative impact on GDP for Korea for sure and also suggests global demand weakness. Usually it takes 4-5 quarters for semiconductors to come out of their downward cycle, thus the bottom hasn’t come yet.”

A screen shows stock information in Toronto's financial district on Jan. 7, 2021.CARLOS OSORIO/Reuters

Canada is facing growing economic headwinds as key trading partners teeter on the brink of recession, piling worries about trade and commodity prices on top of concerns about the domestic economy.

Global growth is being hit on multiple fronts. Central banks around the world, led by the U.S. Federal Reserve, are raising interest rates at the fastest pace in decades – intentionally slowing their economies to fight inflation.

The European energy crisis escalated this week, with the apparent sabotage of the Nord Stream pipelines that ship gas from Russia to Europe. Meanwhile, Britain is in the midst of a currency and bond market meltdown, which pushed the Bank of England to intervene in markets Wednesday and warn of a “material risk to U.K. financial stability.”

The Organization for Economic Co-operation and Development said earlier this week it expects the world economy to be US$2.8-trillion smaller in 2023 than it projected a year ago. And things could get a lot worse, the OECD warned, if a cold winter in Europe leads to energy rationing and new gas supplies fail to materialize.

None of this bodes well for Canada’s trade-oriented economy. Most debate about a potential recession here revolves around domestic issues, including the impact of Bank of Canada rate hikes on the housing market and the amount of savings consumers have built up.

But with forecasters projecting a sharp slowdown in economic growth through the rest of 2022 and into 2023, a fall in foreign demand for Canadian exports or further drops in commodity prices could tip the economy into recession.

“The growth we’re calling for is so slim, that given the risks that are out there, there’s really not a whole lot of margin for manoeuvre,” said Stuart Bergman, chief economist at Export Development Canada.

The crucial variable for Canada is what happens in the United States. There, the outlook has darkened over the past week as the Fed doubled down on its efforts to curb demand in the U.S. economy and get prices under control.

The Fed raised its benchmark interest rate by 0.75 percentage points last Wednesday, to a range of 3 per cent to 3.25 per cent. The rate hike was expected. But updated projections showed policy makers expect to push the Fed Funds rate to between 4 per cent and 4.5 per cent by the end of the year – considerably higher than previously forecast.

“That materially raises the risks that the U.S. economy has a hard landing. And if the U.S. has a hard landing, I think it’s very hard for Canada not to have one as well,” said Craig Alexander, chief economist at Deloitte Canada.

Even Fed chair Jerome Powell acknowledged the central bank was pushing monetary policy into risky territory. “No one knows whether this process will lead to a recession or, if so, how significant that recession would be,” he said in a news conference after last week’s rate announcement.

A U.S. recession would hit a range of Canadian exporters, particularly those tied to interest-rate-sensitive sectors. Lumber and building supply companies would be slammed by a slowdown in American home construction. Automakers and other durable goods manufacturers would be hurt by a pullback in U.S. discretionary spending.

This could be cushioned somewhat by a weaker Canadian dollar. The currency has already lost ground against the U.S. dollar as investors have flocked to U.S. assets as a safe haven, and markets have bet the Fed will raise interest rates more than the Bank of Canada does. A weaker Canadian dollar, in turn, makes Canadian exports more attractive to American buyers.

“The dominant effect is still likely to be the weakening in demand. So Canadian exports will still soften,” Mr. Alexander said. “But the fact that the exchange rate is lower means that Canadian exports won’t fall as far.”

Beyond the U.S., the growth picture is even more dire. China’s economy is expected to grow at the slowest pace in decades this year (excluding 2020 and the COVID-19 shock), as the country struggles with strict pandemic-control measures and a real estate crash.

In Europe, the war in Ukraine and Russian sanctions have sent natural gas and electricity prices soaring. That’s squeezing consumers and making energy-intensive businesses unprofitable, pushing many European Union countries, as well as Britain, toward a period of stagflation: the painful combination of low growth and high inflation.

The OECD now expects the euro area to grow just 0.3 per cent in 2023, down from a projection of 1.6-per-cent growth in June. The German economy is expected to contract 0.7 per cent next year, while the British economy is expected to post no growth.

The energy crisis in Europe presents a mixed outlook for Canadian trade. Some companies will suffer from a drop in demand. But Canada’s trade, broadly speaking, benefits from high energy prices.

“Commodity exporters generally are benefiting at this point from tight global supplies and record high prices across much of the commodity complex,” said Mr. Bergman of EDC, noting that Canadian farmers, miners and energy producers have done well this year.

“And because many countries, especially in Europe, are looking for energy security … exporting these sources are going to offer opportunities for growth,” he said.

Enbridge’s recent US$1.5-billion investment in the Woodfibre LNG terminal in Squamish, B.C., is one such bet on growing global demand for liquefied natural gas. The federal government, for its part, is keen on exporting hydrogen to Germany through East Coast ports, although the infrastructure for this has yet to be built.

These, however, are long-run bets. In the short term, swings in commodity prices could have a bigger impact on trade, and many commodity prices are in retreat. The price of a barrel of West Texas Intermediate crude oil, the North American benchmark, fell below US$80 this week, from a high of US$122 in June. The price of copper, often considered a bellwether for the world economy, has fallen more than 30 per cent since April.

Much depends on how the Organization of the Petroleum Exporting Countries responds to declining global demand for oil.

If OPEC countries, led by Saudi Arabia, curb production, that could keep oil prices relatively high, to the benefit of Canadian energy producers. But other geopolitical factors – including the fate of the Iran nuclear control talks and further limits on Russian oil and gas exports – could also play a major role in energy prices.

“We expect oil to be in for a period of extreme heightened volatility with prices increasingly disconnected from supply demand fundamentals and more driven by headline risk,” EDC’s Mr. Bergman said.

EDC is not yet calling for a recession in Canada or the U.S., and Mr. Bergman said he expects trade to support the Canadian economy through the coming economic turbulence. But he acknowledged the odds of a soft landing are growing increasingly narrow.

“It’s like a bicycle that’s going really, really slowly,” Mr. Bergman said. “It’s fast enough that it’s still staying upright, but it’s kind of wobbling. If it hits a pebble, it could be knocked over. … And there’s a tonne of pebbles around.”

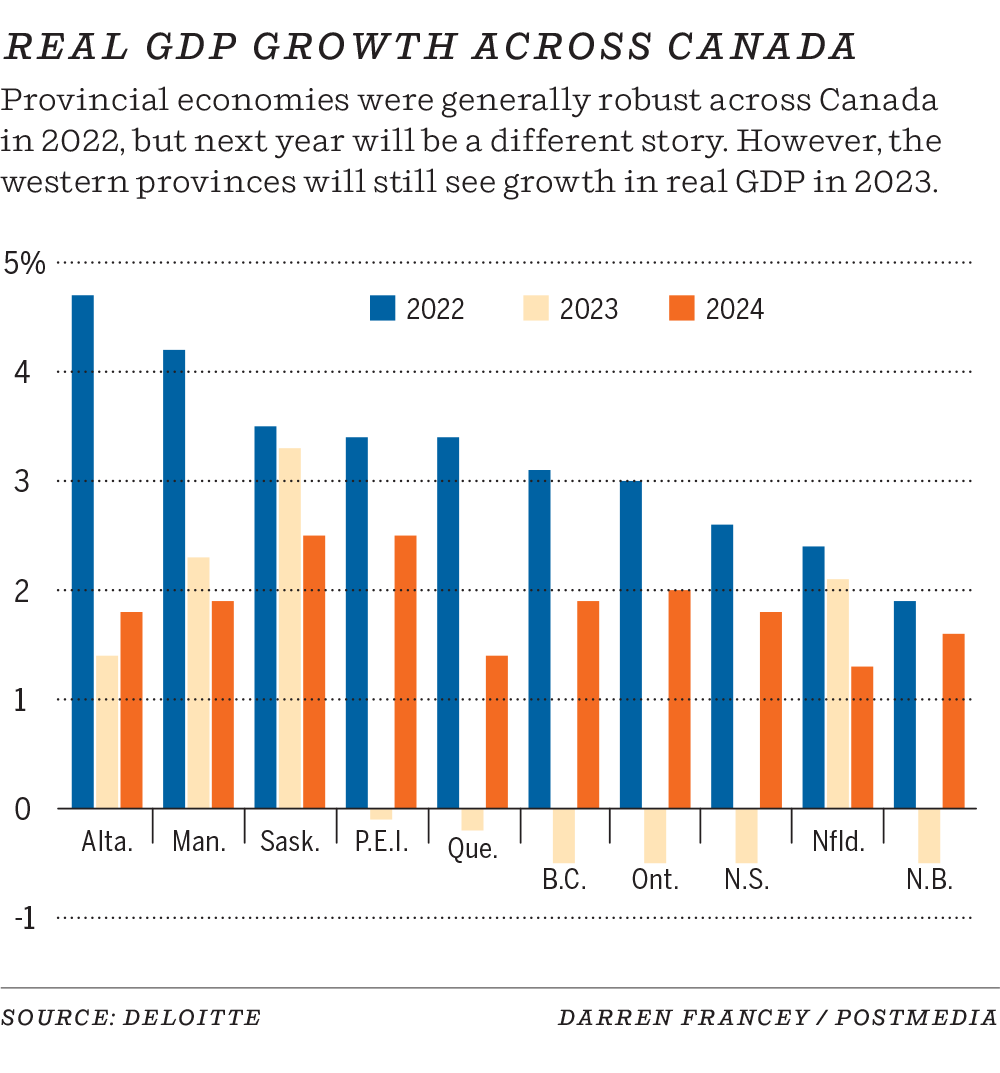

According to Deloitte's latest economic outlook, Alberta will avoid a recession over the next year, a claim Canada will not be able to make as a whole

Downtown Calgary high-rises are framed by the fall-coloured leaves on Wednesday, September 28, 2022.Azin Ghaffari/Postmedia

Article content

Alberta, powered by its resource sector, is expected to be an economic outlier as much of Canada is forecast to slip into recession at the end of this year.

Advertisement 2

Article content

According to Deloitte’s latest economic outlook, released Wednesday, Canada will enter a slight, two-quarter recession in the fourth quarter of 2022 and the first quarter of 2023. Alberta, Saskatchewan and Manitoba, however, are all forecast to maintain positive real GDP growth.

Article content

Alicia MacDonald, senior manager at Deloitte, said it is a reversal of fortune from the recession in 2020, when the Prairies were hit by the pandemic, the bottom dropped out on energy and there were multiple agricultural crises.

Article content

“When we look at 2022 and the prospects this year, we’re really seeing everything kind of come together on those fronts,” she said. “The energy sector, the sharp reversal in fortunes, from a budgetary perspective in Alberta, has been very surprising . . . and that is driven by the oil and gas revenues.”

Advertisement 3

Article content

The outlook has Alberta with the highest real GDP in Canada in 2022 at 4.7 per cent, but slipping to 1.4 per cent in 2023 before rebounding slightly to 1.8 per cent in 2024. Non-Prairie provinces are expected to struggle in 2023 before rebounding to positive growth in 2024 — Newfoundland and Labrador is the exception, with growth expected to mirror the Prairies due to its resource-dependent economy.

Article content

Charles St-Arnaud, chief economist for Alberta Central, said Alberta will likely still experience a considerable slowdown in the economy over the next couple of years, driven by having the third highest consumer debt loads in Canada. With inflation still high and interest rates expected to go up again in October — Deloitte is predicting another 50 basis points — Albertans are expected to exercise more budgetary restraint.

For the retail sector, it could mean a less-lavish Christmas shopping season than hoped.

“Higher costs for everything have been squeezing household budgets,” said St-Arnaud. “There’s a big decline in purchasing power and consumers will have to do some choices in terms of where and how do they spend. There’s some discretionary spending that won’t happen. Big spending on cars, furniture, appliances, might have to be delayed. Part of the slowdown of the economy is that you’ll see weaker consumer spending as we get into the end of the year.”

Advertisement 5

Article content

But data suggests that higher interest rates are starting to have an effect on cooling inflation, though St-Arnaud said the hikes likely are not done — he agrees with the prognostication of a 50-basis-point bump next month and says there could be an additional 25-point increase before the end of this year.

“We saw some moderation in recent months, but that was mainly due to an easing in gasoline prices,” said St-Arnaud. “(The Bank of Canada) still needs to continue to increase interest rates, but we’re getting to that peak in terms of how much they’ll increase.”

Alberta remains one of the most affordable provinces in the country, which is credited with continued net positive interprovincial migration. In the second quarter of 2022, the total was 9,857 for a fourth-consecutive quarter of positive results. In that time, 23,132 Canadians relocated to Alberta; 15,208 in 2022.

Advertisement 6

Article content

Jobs, Economy and Innovation Minister Tanya Fir said that migration is critical to the growth of the economy, to fill gaps in the labour force.

“It’s so important to have people coming in,” she said. “All of these industries, whether they’re the traditional ones or the more growing and emerging ones, are going to need the skilled workers. These positive migration numbers are a great indication that our goal to get these skilled positions filled is going to come to fruition.”

The last time there were four consecutive quarters of net-positive interprovincial migration to Alberta was the third quarter of 2014 to the second quarter of 2015 — also the last time there were four-digit positive gains.

Fir pointed to affordable housing, lower taxes and diversified job opportunities as the draws. Many people are coming to Alberta from Ontario and B.C., where the province has rolled out its Alberta is Calling campaign.

Advertisement 7

Article content

While oil and gas remain the province’s main economic drivers, other sectors have also begun to pick up the slack, including film and television production, record investment in the tech sector, a rebound in agriculture and a growing service industry.

One positive of the impending slowdown is Deloitte is not expecting employment to bottom out, as it often does in a recession. MacDonald said the current tight labour market will help mitigate some of these pains.

“If you’re looking at laying off staff, you have to ask yourself, ‘how easy is it going to be to get these staff back when demand starts to pick back up?’ ” she said. “We think employers are going to hold on to their employees a lot longer than they normally would during a period of slowdown, just because it’s been so difficult to find the right skills for the jobs that are out there.”

(Bloomberg) -- Citadel’s billionaire founder, Ken Griffin, said the US equity market is showing resilience thanks to a healthy labor market and strong consumer confidence.

Speaking on Wednesday at the CNBC Delivering Alpha conference in New York, Griffin said Citadel is “very focused on the possibility of a recession,” but he struck a less bearish tone than fellow speakers such as Duquesne Family Office founder Stan Druckenmiller, who predicted that one will happen next year.

“The US economy is still strong for people who are going to work every day. In fact I think we’re looking at real wage growth in Q4 this year,” Griffin said.

Consumers are spending more on things like airlines and electronics, which creates “a real powerful tailwind” to the overall economy, he said. “So the forward trajectory on a number of key fronts looks somewhat better domestically, assuming nothing goes totally off the rails.”

The Citadel founder said he thinks the typical 60/40 portfolio of stocks and bonds “is much better today than at any point in recent time.”

Still, the US Federal Reserve has a difficult job ahead of it in using a “blunt tool” -- interest rates -- to address an overheated economy, Griffin said. He said the Fed should continue on its rate-hike path to “re-anchor” inflation expectations.

The comments come as stocks are rallying after the Bank of England pledged on Wednesday to buy long-dated government bonds in whatever quantities are necessary to restore order to the markets. Wednesday’s gains followed a weeklong rout in US stocks amid central-bank moves intended to fight inflation. Last week, the Federal Reserve hiked interest rates for the third straight meeting and signaled a fourth such increase is likely in November.

Citadel’s flagship Wellington fund gained about 21% this year through July, Bloomberg previously reported. When asked about the fund’s strong performance, Griffin said the vehicle is highly fluid and has made several on-point short-term calls over the past nine months. Energy in particular “has been an unbelievable trajectory” for most of 2022, he said.

Griffin added that another advantage for Citadel has been that its entire team is back at work. Griffin has been a staunch advocate of having staff work in-person, with the firm ranking among the first hedge funds to bring employees back to their desks.

Griffin recently moved his family and businesses to Miami, becoming Florida’s wealthiest person. He’s spent hundreds of millions of dollars on two homes in the state and is shifting Citadel’s headquarters to the Brickell neighborhood from Chicago.

Griffin said it’s “really fun” to be in an environment where “people embrace the future and are hopeful about tomorrow,” while conversations in Chicago are often about the city’s high crime rate.

In the House of Commons, when members of Parliament become rowdy, the Speaker will often bellow ‘Order, Order!’ Much of the same treatment is needed for gilts and sterling, both moving in a violent manner that historically has typified the breakdown of an economic regime.

There are several lessons to be learned here – one of which is that when making policy there is a need to be cognizant of the broader economic and financial environment. A financial climate troubled by inflation, rising interest rates and dangerous geopolitics is not one in which mistakes will be tolerated.

The early schoolboy/girl errors of the Truss government mark the cumulative effect of a long process of policy neglect and geopolitical decline. The death of Queen Elizabeth II has, amongst many other things, contributed to the sense that an era has passed, and that a new, more testing one is upon us.

Brexit

Wrapped up in all this is the Brexit project, which has drained U.K.’s economy of its vitality (investment, productivity and growth have stalled badly), exhausted the patience of Britain’s international partners and debased the political climate in the U.K. That Brexit is not working is a clear message from financial markets.

Another longer-term message is that Britain’s outsized role in the international economy and world stage is now over. Some years ago, the economist Barry Eichengren produced a paper that showed that through history, as empires have declined, so too has the role their currency has played in the international economy. This has led some to posit that the dollar should start to waken as we enter a multipolar world. If Britain does prove this theory correct, there should be a long lag to dollar weakness, if that is to happen, but the lag will be long. Bear in mind that at the time of the American Civil war, one pound bought ten dollars, and this fell to four at the time of the Suez crisis and, collapsed to one now.

Lessons of Small States

A further source of comfort for Americans is that unlike the U.K., the U.S. is not breaking up. In Britain, Brexit has detonated history such that Scottish independence is now likely in the next five to ten years, the reunification of Northern Ireland and the Republic is widely discussed, and there is even an upswing in Welsh independence sentiment.

Looking ahead, the chief issues now are in the short term whether economic and financial volatility will persist, and by association whether the Truss government survives its experiment with an economic model that appeared to work in 1980’s America, and then more challengingly, what becomes of the idea of Global Britain, and logically the ‘Little Britain’ that Liz Truss appears to be trying to create.

In the short term, there are two obstacles – the volatile financial market outlook and the rupture in the credibility of Britain as an investment destination, and a major economy (for comparison – British 10 year bond yields are 4% (helped lower by renewed buying by the Bank of England) whereas that of its neighbor Ireland trade at 2.7%).

In particular the reputation of the Tories as the stewards of the economy is in smithereens. The Tories face ongoing questions regarding their closeness to Russian money, and to the London hedge funds that shorted sterling.

In the longer term, the U.K. needs at least two changes of tack. The first is an economic model akin to that of small, advanced economies like Sweden, Singapore and Switzerland that priorities access to good education and public goods, focuses on the drivers of productivity, values the rule of law, good institutions and the people who run them (the sacking of Sir Tom Scholar from the Treasury was significant in this regard). In my view, it is unlikely that Britain will adopt this approach, even though it has been shown to produce high quality long-term growth in a range of countries (The Lessons of Little States).

The second changes relates to the political system. The distasteful chaos of the Johnson premiership and the incompetence of the Truss one have resulted in a sizeable lead in the polls for Labour. Should they come to power in a subsequent election, one choice that may confront them is electoral reform.

Introducing proportional representation in the place of the first past the post system would radically alter British politics – it would force collaboration, more coalitions and arguably foster a more policy focused debate. Importantly it would make it easier for parties to evolve. Brexit is largely the result of deep internal divisions within the Tory party that poisoned national politics because there was no suppleness in the party system.

Such a change might reestablish growth, and a sense of ‘order’ in Britain.

OTTAWA, Sept. 28, 2022 (GLOBE NEWSWIRE) -- A report released today by the Canadian Climate Institute shows that the mounting costs of a volatile climate are already dragging down Canada’s economy, with these costs rising swiftly in the coming years. The report—Damage Control: Reducing the costs of climate impacts in Canada—examines the macroeconomic costs of climate change, assessing them in both low- and -high emissions scenarios relative to a stable-climate scenario. The analysis shows that climate impacts will cost Canada billions, making life less and less affordable for households as economic growth slows, governments raise taxes to pay for climate disasters, job losses increase, and goods become more expensive due to disrupted supply chains.

The report, which is a culmination of a five-report series and the most comprehensive macroeconomic analysis of climate change in Canada to date, also presents solutions. Proactive adaptation measures and policies can limit climate change damage, cutting the projected costs in half, saving billions of dollars, and making life more affordable for households. A dollar invested in proactive adaptation measures, the report finds, can return $13-$15 in direct and indirect benefits. And if adaptation measures are combined with global emissions reductions, future costs could be reduced by three-quarters, putting Canada on a path to a more stable and affordable future.

Key findings fromDamage Control:

Climate-induced damages are already here and they’readding up. By 2025, climate impacts will be slowing Canada’s economic growth by $25 billion annually, which is equal to 50 per cent of projected GDP growth.

All households will lose income, and low-income households will suffer the most. Low-income households could see income losses of 12 per cent in a low emissions scenario and 23 percent in a high emissions scenario by the end of the century.

Climate change is a job-killer. Job losses could double by mid-century, and increase to 2.9 million by end-of-century.

Adaption pays off big. Every dollar spent on adaptation measures saves $13-$15, including both direct and indirect economy-wide benefits.

Limiting further warming, while adapting to the warming already baked in, pays off bigger. Taking proactive adaptation measures cuts climate costs in half, and if these are combined with global mitigation measures, then costs are cut by three-quarters.

QUOTATIONS

“The findings couldn’t be clearer: Canada is directly in the crosshairs of a changing climate. The economy is highly sensitive to this threat, and we’re already paying the costs: as early as 2025, the damages will have cut Canada’s growth rate in half. We need to reckon with these massive costs and do everything we can to limit the damage.”

—Dave Sawyer, Principal Economist, Canadian Climate Institute

“The cost of inaction when it comes to climate change is measurable and mounting. We need to put adaptation and mitigation measures in place now to avoid severe damage to our economy, society, health, and well-being.”

—Rick Smith, President, Canadian Climate Institute

“The economic consequences of climate change are only now coming into view, and this report provides thoughtful insights on just how climate change could impact the Canadian economy. The threat is real, but, fortunately, there’s much that can be done to limit the damages. Investing in adaptation and resilience today will help protect Canada’s economy and could save lives. Taking proactive adaptation measures can cut the costs of climate change impacts and provide a strong return on investment, saving money in the long-term while paving the way for a more sustainable and prosperous future for Canadians.”

—Susan McGeachie, Head of BMO Climate Institute, BMO Financial Group

(Reuters) - San Francisco Federal Reserve Bank President Mary Daly said on Tuesday that the U.S. central bank is "resolute" about bringing down high inflation but also wants to do so "as gently as possible" so as not to drive the economy into a downturn.

It is important, Daly said at a symposium held jointly with the Monetary Authority of Singapore, "to navigate through this high inflation environment as carefully as we can, so that we don't leave longer term damage to our labor market."

(Reporting by Ann Saphir; Editing by Christian Schmollinger)

Is the economy headed for a hard or a soft landing? That’s the question on a lot of people’s minds following the Federal Reserve’s third and most recent interest rate hike last week. And it’s the question former U.S. Treasury Secretary Lawrence Summers and current President of the Federal Reserve Bank of Minneapolis Neel Kashkari answered during an online economic outlook question-and-answer session hosted by the Wall Street Journal Tuesday.

Below are excerpts from their conversation:

Is the Fed committed to aggressive rate hikes to defeat inflation?

Kashkari: “The only other time I have seen us this united was at the beginning of the pandemic, when we knew we had to act boldly to support the economy through the pandemic and through the downturn. We are all united in our job to get inflation back down to 2%, and we are committed to doing what we need to do in order to make that happen. And that leads to more tightening of monetary policy in the near term. Ultimately, how much we need to do is not just up to us. It’s going to be determined also by the supply side of the economy and whether we get some help on the supply side.”

Is the Fed overdoing it with rate hikes?

Summers: “No. I think the Fed allowed itself to get way behind the curve for a long time in 2021 early 2022 and in the process sacrificed a reasonable amount of credibility. And in that context, it is necessary to move very strongly and to be very clear and straightforward… We do absolutely need to do what’s necessary to bring inflation substantially down, and the more determination with which that’s done, the less painful the process is likely to be. Of course, there’s a risk that it will be overdone, but certainly at the current level of a 3% Fed funds rate … I certainly don’t think it’s been overdone yet.”

What should the Fed be looking at to decide when the Federal funds rate is at the right level?

Summers: “I would be watching very carefully what was happening in the labor market. I’d be looking for evidence that signs of an overwhelmingly tight labor market were giving way to signs of a labor market with more slack. I would be looking at a broad range of price increases to see whether in the median price we were starting to see a substantial decline in inflation. I would be looking at the kind of reports that the Fed gets on everything from future hotel reservations to business orders for a sense that a precipitous recession was starting to break out.”

What are the odds of American financial asset prices remaining low for a longer time?

Summers: “If one looks at asset prices, they seem to factor fully in what’s happened to real interest rates. I’m not sure the kind of earnings that would be likely to accompany a recession, if we have one, is something that’s fully factored into asset prices at this point.”

Is the economy in for a soft landing or a harder, longer recession?

Kashkari: “I think a soft landing is still possible, and certainly we will work very hard to try to achieve it, but a lot of it is out of our control. Do we get more help on the supply side of the economy or is bringing the economy into balance entirely up to reducing demand, and that’s through the Federal Reserve. If that’s the case, then it’s much more likely to be a hard landing. And so we are going to try to achieve a soft landing, but we are going to get inflation back down to 2%.”

Summers: “I think a hard landing is substantially more likely than a soft landing. If inflation is going to come down in two or three years … that’s likely to be in the context of a recession, not in the context of a smooth path. Neel said that unless we get a miracle on the supply side, or unless we get a lot of happy news on the supply side, it’s likely to be a hard landing. I think that’s right, and I don’t know what reason there is for thinking that we are going to get some kind of sudden major increase in productivity.”

The Washington-based lender expects the region to grow 3.2 percent in 2022, down from a 5 percent forecast in April.

The World Bank has slashed its economic outlook for the Asia-Pacific, pointing to China’s ultra-strict “zero-COVID” policy as a drag on regional growth.

The region’s economies are expected to grow 3.2 percent in 2022, down from a 5 percent forecast in April, as China’s lockdowns continue to disrupt factories and dampen spending, the Washington-based financial institution said on Tuesday.

China, the world’s second-largest economy, is projected to grow 2.8 percent this year, according to the bank, and 4.5 percent in 2023.

The lender previously predicted China would grow 5 percent in 2022.

Despite the rest of the world’s moves towards living with the coronavirus, China has stuck to a zero-tolerance strategy aimed at stamping out the coronavirus at almost any cost.

The World Bank also pointed to aggressive interest rate hikes by central banks trying to curtail soaring inflation as a risk to the region’s growth.

“As they prepare for slowing global growth, countries should address domestic policy distortions that are an impediment to longer term development,” World Bank East Asia and Pacific Vice President Manuela Ferro in a statement.

HALIFAX - While the damage caused by post-tropical storm Fiona is still being assessed across Atlantic Canada, it’s become clear the economic fallout will be substantial for some parts of the region.

Elmwood, P.E.I., potato farmer Alex Docherty estimates his farm suffered losses of about $500,000 following the weekend’s storm. In an interview Monday, Docherty said three of his storage buildings were destroyed by hurricane-force winds, as were the barns of several nearby farmers.

“If a bomb went off, I don’t know whether it would do any more damage,” Docherty, owner of Skyview Farms, said. “On my road within a mile of me there’s nine barns down — you’d swear it’s a war zone.”

The storm made landfall as farmers were getting ready to harvest their potato crops, he said. The ongoing blackouts across many parts of the province, he added, risk causing storage problems because the potatoes need to be kept cool.

The Island’s agriculture industry is facing a “huge” hit, Docherty said.

Premier Dennis King said that while it’s too early to know the extent of the economic fallout caused by Fiona, it’s expected to be major given the damage to the farming and fishing industries and to a number of businesses, which have been forced to close.

“We will measure it in the millions I’m quite sure,” King said in a briefing Monday.

The premier said there has been significant damage to some mussel and oyster farming operations and he’s waiting to hear about the state of lobster traps. In agriculture, “soybeans and corn took a beating and our apple farms have as well,” King said.

In Sydney, N.S., Marlene Usher, chief executive of the city’s port, said she had to tell three cruise ships on Monday that they shouldn’t come this week. Usher said a total of 12 cruise ships have cancelled their arrivals because of Fiona, for a loss of well over $1 million to the port and various local businesses.

Standing at the reception centre of the port, where electricity had just returned, she said that after several poor seasons due to COVID-19, it’s hard to lose more customers in the prime fall season when ships come to the harbour with thousands of tourists.

“The Port of Sydney’s main revenue generator is the cruise ships … we were already in a serious situation in terms of revenues and reserves at the port. We manage our costs, but this puts us in a precarious situation,” Usher said.

Andrew Prossin, the owner of a small, 100-passenger vessel that tours Sydney harbour, said in an interview that his business has also taken a hit. “All the local tour operators are standing by, and that in and of itself is tough … to keep the engines idling. There will be an impact from the loss of the key business this time of year.”

Usually, the most profitable time of year for marine tourism is September and October, Prossin said, adding that between 60 and 70 per cent of his revenues comes in those months.

In a video news conference Monday, Nova Scotia Premier Tim Houston said it’s anticipated the economic damage from Fiona will be greater than previous storms. Houston also announced about $40 million in provincial aid to people directly affected by the storm.

“Disaster relief funding will be helpful for uninsured losses, but we know this may take time and there will be gaps,” the premier said.

Paul Kovacs, executive director of the Institute for Catastrophic Loss Reduction at Western University, said the benchmark for destruction in the region is the $200 million worth of insurable losses caused by hurricane Juan in 2003.

Kovacs believes it’s time there was a conversation involving governments about what can be done to better prepare for increasingly violent storms linked to climate change. He said research has shown that building stronger, wind-resistant homes, for instance, can make a difference. Kovacs said the state of Florida changed its building code 15 years ago to impose tougher construction standards.

Kovacs said it can be relatively inexpensive to strengthen the connection of a roof to a wall or of a foundation to a wall while constructing a new home. “Lets start preventing the damage,” he said. “Let’s spend the money upfront so we avoid the damage down the road.”

This report by The Canadian Press was first published Sept. 26, 2022.

SHARE:

JOIN THE CONVERSATION

Anyone can read Conversations, but to contribute, you should be registered Torstar account holder. If you do not yet have a Torstar account, you can create one now (it is free)

Sign In

Register

Conversations are opinions of our readers and are subject to the Code of Conduct. The Star does not endorse these opinions.

Communist China under premier Xi Jinping is wilting fast.

The economy, already under pressure so far this year, looks set to get even worse, according to a recent report from London-based consulting firm Capital Economics.

Capital kicks off with the following blistering assessment of the situation:

“The financial world’s focus on a generational surge in inflation in advanced economies is stealing attention from a generational slowdown in China that is arguably of much greater importance for the long-term global outlook.”

In other words, ignore China’s economic worsening quagmire at your peril.

Already we know that China’s steel production is falling, down 5.7% in the year through August, according to the World Steel Association. That country has long been the world’s largest producer of steel so the decline is meaningful on a global scale.

Worse still, only two of the top global producers performed worse over the same period: Russia and Turkey. Both are economic basket cases.

The hits keep on coming. Exports from Korea to China fell during the first three weeks on September, the Capital report says. At the same time, Korean exports to the U.S. grew.

“This may be a sign that global demand for the consumer goods that China produces – and to which Korea provides inputs earlier in the production chain – is softening,” the Capital report states. My emphasis.

Put simply, retail customers globally are pulling back and thats already hurting China.

Monthly data for August show declining retail sales inside China as well and Capital expects further declines in September.

When the experts put all this together the outlook is bleak.

“We recently lowered our forecast for this year’s officially-reported GDP growth rate to 3% from 4% – the government’s 5.5% target set in March has been quietly abandoned – but in reality don’t expect the Chinese economy to grow at all.”

Put another way, China’s growth under Xi likely dropped to zero from regular double-digit gains.

It’s not the sort of achievement most leaders want.

PARIS, Sept 26 (Reuters) - Global economic growth is slowing more than was forecast a few months ago in the wake of Russia's invasion of Ukraine, as energy and inflation crises risk snowballing into recessions in major economies, the OECD said on Monday.

While global growth this year was still expected at 3.0%, it is now projected to slow to 2.2% in 2023, revised down from a forecast in June of 2.8%, the Organisation for Economic Cooperation and Development said.

The Paris-based policy forum was particularly pessimistic about the outlook in Europe - the most directly exposed economy to the fallout from Russia's war in Ukraine.

Global output next year is now projected to be $2.8 trillion lower than the OECD forecast before Russia attacked Ukraine - a loss of income worldwide equivalent in size to the French economy.

"The global economy has lost momentum in the wake of Russia's unprovoked, unjustifiable and illegal war of aggression against Ukraine. GDP growth has stalled in many economies and economic indicators point to an extended slowdown," OECD Secretary-General Mathias Cormann said in a statement.

The OECD projected euro zone economic growth would slow from 3.1% this year to only 0.3% in 2023, which implies the 19-nation shared currency bloc would spend at least part of the year in a recession, defined as two straight quarters of contraction.

That marked a dramatic downgrade from the OECD's last economic outlook in June, when it had forecast the euro zone's economy would grow 1.6% next year.

The OECD was particularly gloomy about Germany's Russian-gas dependent economy, forecasting it would contract 0.7% next year, slashed from a June estimate for 1.7% growth.

The OECD warned that further disruptions to energy supplies would hit growth and boost inflation, especially in Europe where they could knock activity back another 1.25 percentage points and boost inflation by 1.5 percentage points, pushing many countries into recession for the full year of 2023.

"Monetary policy will need to continue to tighten in most major economies to tame inflation durably," Cormann told a news conference, adding that targeted fiscal stimulus from governments was also key to restoring consumer and business confidence.

"It's critical that monetary and fiscal policy work hand in hand", he said.

Though far less dependent on imported energy than Europe, the United States was seen skidding into a downturn as the U.S. Federal Reserve jacks up interest rates to get a handle on inflation.

The OECD forecast that the world's biggest economy would slow from 1.5% growth this year to only 0.5% next year, down from June forecasts for 2.5% in 2022 and 1.2% in 2023.

Meanwhile, China's strict measures to control the spread of COVID-19 this year meant that its economy was set to grow only 3.2% this year and 4.7% next year, whereas the OECD had previously expected 4.4% in 2022 and 4.9% in 2023.

Despite the fast deteriorating outlook for major economies, the OECD said further rate hikes were needed to fight inflation, forecasting most major central banks' policy rates would top 4% next year.

With many governments increasing support packages to help households and businesses cope with high inflation, the OECD said such measures should target those most in need and be temporary to keep down their cost and not further burden high post-COVID debts.

Reporting by Leigh Thomas, additional reporting by Tassilo Hummel; editing by Richard Lough, William Maclean

(Bloomberg) -- The world as a whole has been jolted by the war in Ukraine, according to the OECD, which cut almost all growth forecasts for the Group of 20 next year while anticipating further interest-rate hikes too.

The global economy will expand just 2.2% in 2023, the Paris-based organization said Monday. It slashed GDP forecasts for most of the G-20, with only Indonesia featuring a moderately higher outlook. Many of the group face noticeably faster inflation too.

“The global economy has been hit,” the OECD said in interim forecasts. “The world, and Europe in particular, is bearing the cost of the war in Ukraine, and many economies face a difficult winter.”

The outlook provides a snapshot of the synchronized shock stemming from Russia’s attack on Ukraine and the ensuing energy crunch that has inflicted a widespread cost-of-living crisis.

Global central banks have delivered rate hikes this month adding up to more than 2,000 basis points combined to fight soaring consumer prices. That’s not yet enough, according to OECD officials.

“Inflation has become broad-based in many economies,” they said in the report. “Further interest-rate increases are needed in most major economies to anchor inflation expectations and ensure that inflation pressures are reduced durably.”

The growth hit is particularly visible in Europe. The OECD now expects Germany, the region’s biggest economy, to contract 0.7% next year.

“In Europe, many economies are likely to have at best weak growth in the second half of 2022 and the first quarter of 2023 before some improvement through the remainder of 2023,” according to the report.

Officials predict “near-term output declines” in Germany, Italy, the UK and “the aggregate euro area, given the drag exerted by declining real incomes and the disruptions in energy markets.”

The OECD highlighted the “significant uncertainty” surrounding its projections, which assume the absence of further Covid waves, no escalation or broadening of the war in Ukraine and a calming down of energy-market pressures.

“EU gas storage levels have been raised considerably through the course of this year, and are now between 80-90% on average in most member states,” the OECD said. “Even at this level, there may not be sufficient storage to ensure that demand in a typical winter can be met without storage levels in the European gas market being pushed below effective operational levels.”

More severe fuel shortages, especially for gas, could reduce growth in Europe by a further 1.25 percentage points in 2023 and raise inflation by over 1.5 percentage points, the OECD said, pushing “many countries into a full-year recession in 2023” and European growth “would also be weakened in 2024.”

The report also showed:

In China, growth will slow to 3.2% this year amid repeated Covid-19 shutdowns and a crisis in the property market, “but policy support could help growth recover in 2023,” the OECD said

The US economy will grow just 0.5% next year

Fiscal support is required to “help cushion the impact of high energy costs on households and companies,” but it must be “temporary, concentrated on the most vulnerable, preserve incentives to reduce energy consumption and be withdrawn as energy price pressures wane”

Food security remains under threat because of the war and international cooperation is required to “keep agricultural markets open, address emergency needs and strengthen supply”

(Bloomberg) -- Brazilians’ views on the economy are improving amid stronger-than-expected activity and easing inflationary pressures.

The number of voters who believe the economy is doing better now is as high as before the onset of the Covid-19 pandemic, local newspaper Folha de Sao Paulo reported on Sunday, based on the latest Datafolha poll. In the survey, 28% of respondents say the economic outlook has improved, up from 25% in August and 15% in June. Still, 50% believe activity has worsened in the last few months.

Latin America’s largest economy is witnessing the first signs of easing inflationary pressures. Consumer prices fell back to single digits in August, after tax cuts on gasoline prices kicked in and commodity prices declined. Activity is proving resilient to an aggressive monetary tightening campaign, as unemployment fell for five consecutive months amid stronger-than-forecast growth in the second quarter.

President Jair Bolsonaro’s voters have a more positive view on the economy, with 64% saying there’s an improvement in recent months. Only 7% think alike among those who favor former president Luiz Inacio Lula da Silva, still the favorite ahead of presidential elections.

Read More: Bolsonaro Becomes Main Target in Brazil Debate Without Lula

The economy remains one of the top concerns for Brazilians as they head to the polls on Oct. 2. Trying to improve his chances of reelection, the incumbent pushed a multibillion social package that included boosted paychecks to the poor. Still, 55% of those who received the aid believe the economic outlook is worse now, with 46% saying their personal situation also worsened in recent months.

Read More: Bolsonaro, Lula Battle for Votes in Brazil’s Largest State (2)

Both Bolsonaro and Lula are focusing on populous regions of the country in the week before the election day. Bolsonaro is continuing to reach out to female voters, while Lula is facing a tough fight with his opponent among evangelical groups.

This week FP’s top videos turn the spotlight on the economy and how Canadians are coping in uncertain times.

Article content

What Canada needs to get economy on track

Anne McLellan, a senior advisor for Bennett Jones LLP and former federal cabinet minister, talks to Financial Post’s Larysa Harapyn about Canada’s shortcomings and her work on the Coalition for a Better Future, a group that is developing a new economic and social plan for the country.

Don’t see Fed slowing down this year: Canaccord Genuity

Chris Kerlow, senior portfolio manager & investment adviser at Canaccord Genuity Corp., talks about how central banks’ fight against inflation with aggressive rate hikes is affecting markets and the economy.

Inflation data this past week cooled for the second month in a row. What will that mean for consumers and interest rates? The Financial Post’s Stephanie Hughes breaks it down.

We apologize, but this video has failed to load.

Pros and cons of fixed vs variable mortgage rates

Mortgage broker Leah Zlatkin explains the pros and cons of fixed vs variable mortgage rates as borrowing rates tick steadily higher.

We apologize, but this video has failed to load.

Listen to Down to Business for in-depth discussions and insights into the latest in Canadian business, available wherever you get your podcasts. Check out the latest episode below:

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/tgam/ZNO4LMSGZFJONNPJZS2KNJXAZI.JPG)

:format(webp)/https://www.therecord.com/content/dam/thestar/business/2022/09/26/atlantic-canadas-economy-likely-to-take-big-hit-from-post-tropical-storm-fiona/2022092613098-6331dc9e3719bf2b1a311844jpeg.jpg)

/cloudfront-us-east-2.images.arcpublishing.com/reuters/W32BHJL2OFLK5PEU5MJO7N6ZPA.jpg)