People shoping at Saras Ajeevika Mela, organised by Ministry of Rural Development at Noida Haat, Sector 33 on February 27, 2022 in Noida, India.

Hindustan Times | Hindustan Times | Getty Images

India's economy lost momentum in the final quarter of 2021, with growth slowing from previous two quarters, data showed on Monday, as fears mount that soaring costs in the wake of Russia's invasion of Ukraine will further sap growth.

Gross domestic product rose 5.4% year-on-year in October-December, official data showed, less than 6% forecast by economists in a Reuters poll, and below upwardly revised 8.5% growth in July-September and 20.3% April-June expansion.

"The growth number is really disappointing," said Sujan Hajra, chief economist at Mumbai-based Anand Rathi Securities, citing weakening rural consumer demand and investments.

India, which covers nearly 80% of its oil needs through imports, possibly faces a widening trade deficit, a weaker rupee and higher inflation after crude prices spiked above $100 a barrel, with a hit to growth seen as the main concern.

"Given the geopolitical instability and crude oil prices, we think the fiscal and monetary policy accommodation will continue," Hajra said.

A 10% rise in oil prices could shave 0.2 percentage points off India's GDP growth while adding 0.3 to 0.4 percentage points to retail inflation, according to Nomura's estimates.

The Reserve Bank of India slashed its key repo rate by 115 basis points since March 2020 to soften the blow from the coronavirus pandemic and has kept rates low to support the economic recovery.

Weakening demand

However, that recovery, already sputtering amid weak consumer demand and private investment, slowed further when the third wave of coronavirus infections hit Asia's third-largest economy last month.

Growth in consumer spending, its main driver, slowed to 7.0% from a year earlier in October-December quarter from revised 10.2% in previous quarter, Monday's data showed.

Manufacturing slowed to 0.2% growth from revised expansion 5.6% expansion in the previous quarter while the construction sector contracted 2.8% after 8.2% growth in the previous quarter.

The government also cut its growth estimate for the 2021/22 fiscal year ending on March 31 to 8.9% from 9.2% seen in January as Covid-19 related curbs weighed on activity early this year.

Investment growth slowed to just 2.0% on year compared with revised 14.6% increase in the previous quarter, with state spending slowing to 3.4% growth after a 9.3% rise in July-September.

Sakshi Gupta, senior economist at HDFC Bank, said India was likely to feel the ripple effects of widening sanctions against Russia.

"We see a downside risk of 20-30 basis points to our base forecasts," she said. For now HDFC sees the economy growing 8.2% in the next fiscal year.

People stand in line to use an ATM money machine in Saint Petersburg, Russia February 27, 2022.

Register now for FREE unlimited access to Reuters.com

LONDON, Feb 28 (Reuters Breakingviews) - Fortress Russia is crumbling. The central bank more than doubled its main policy interest rate to 20% on Monday to support the plunging rouble. It won’t be enough given Moscow has a dearth of palatable policy options.

The rouble fell as much as 23% against the dollar at the first chance traders had to react to some Russian banks’ imminent ejection from the SWIFT payments system as well as restrictions on central bank reserves. Those Western sanctions shattered the impression that Moscow had large enough economic buffers to withstand whatever America and its Western allies might throw its way.

Those defences had been built up since 2014, when President Vladimir Putin annexed Crimea. Russia runs a budget surplus and has total external debt of only around $478 billion, or about a third of GDP. It had amassed more than $630 billion in central bank reserves read more and around $174 billion in the National Wealth Fund that grows when energy prices rise. Lenders like Sberbank (SBER.MM) were well capitalised and not reliant on foreign funding.

Register now for FREE unlimited access to Reuters.com

All that went out the window over the weekend. Sanctions make it less certain that large revenues from energy exports will keep rolling in. The central bank’s massive rate rise was of temporary help but won’t be enough to stop Russians from trying to convert their savings into foreign exchange or withdraw money out of banks altogether. That’s why Sberbank’s global depository receipt lost more than two-thirds of its value in London trading, even as the Moscow market was shut. The European Central Bank, meanwhile, said Sberbank’s subsidiaries in Austria, Croatia and Slovenia were likely to fail.

Central bank boss Elvira Nabiullina said Russia’s internal payments system can connect to international alternatives to SWIFT. Maybe, but that won’t make overseas counterparties any less rouble-averse. She could hike rates a lot higher, but that would hurt a damaged economy. Ramping up capital controls is another option. She has already ordered any attempt by foreigners to sell Russian securities to be rejected. But banning rouble sales outright would paralyse importers. The central bank sold $1 billion propping up the rouble on Thursday but will find it harder to keep going following fresh sanctions which also hit the wealth fund.

Nabiullina’s best efforts won’t prevent the rouble’s collapse from reverberating throughout the economy. For all her past policy successes, it’s not in her power to prevent an economic collapse.

(The author is a Reuters Breakingviews columnist. The opinions expressed are her own.)

CONTEXT NEWS

- Russia’s central bank on Feb. 28 raised its key policy interest rate to 20% from 9.5% as it tried to contain the fallout of Western sanctions imposed in retaliation against Moscow’s invasion of Ukraine.

- The U.S. Treasury on Feb. 28 blocked Americans from engaging in any transactions involving Russia’s central bank, National Wealth Fund and finance ministry.

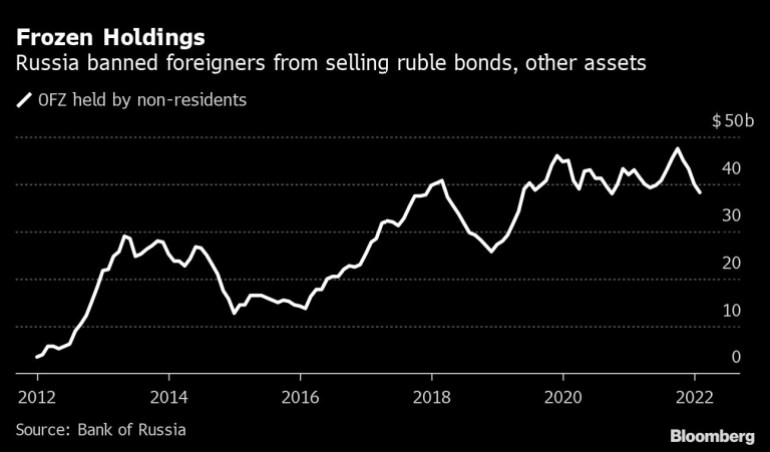

- The Russian central bank also ordered companies to sell 80% of their foreign currency revenue, increased the range of securities that can be used as collateral to get loans and temporarily banned Russian brokers from selling securities held by foreigners. It did not specify to which securities the ban applied.

- On Feb. 27, the central bank said it would resume buying gold on the domestic market, launch a repurchase auction with no limits and ease restrictions on banks’ open foreign currency positions.

- The rouble weakened to 109 against the dollar in early trading on Feb. 28 from 84 late on Friday. It was trading at 98 at 1332 GMT.

- Russia’s stock market was closed but London-traded depositary receipts in Russia’s biggest lender, state-owned Sberbank, fell 69%.

Register now for FREE unlimited access to Reuters.com

Editing by Swaha Pattanaik, Karen Kwok and Oliver Taslic

Budget 2022 is investing more than ever before to help people and communities make the transition to a cleaner, stronger economy through the CleanBC Roadmap to 2030.

With more than $1.2 billion in new funding for CleanBC, Budget 2022 is accelerating actions to strengthen communities and expand opportunities for clean economic growth. The new funding builds on the $2.3 billion previously committed to CleanBC to reduce emissions across sectors.

To help communities reduce pollution and prepare for impacts of climate change, the Province is launching a new local government climate action program, funded through $76 million over three years, that will provide predictable, flexible funding to meet local needs. This is in addition to record commitments of up to $244 million from the Province and federal government for the CleanBC Communities Fund.

The way people get around is also changing: $30 million is helping local governments build active transportation projects like bike lanes and multi-use pathways. This is in addition to $2.7 billion over the fiscal period in new funding for better public transit, such as the Broadway Subway and free transit for children 12 and under.

Communities are also working hard to end waste and cut pollution: $10 million will be invested in CleanBC Plastics Action Plan projects to divert plastic waste and reduce emissions from landfills as part of a plan to expand B.C.’s circular economy initiative.

People are making the switch to electric vehicles at an increasing rate, with vehicle rebates totalling nearly $250 million, to be funded through the Low Carbon Fuel Standard program. In addition, purchases of used zero-emission vehicles are now PST exempt until 2027.

B.C. is a leader in electric vehicles with 13% of all new light-duty vehicle sales last year being zero emission. As part of the CleanBC Roadmap, 90% of all new light-duty vehicle sales in the province will be zero emission by 2030.

Budget 2022 continues support for businesses facing competitiveness pressures as they decarbonize and move toward a net-zero emissions economy. The Province has committed an additional $310 million to help reduce emissions from industry. This includes support for the internationally recognized and award-winning CleanBC Program for Industry to expand the use of clean technology in industry as well as measures to help reduce methane emissions and help make industrial operations "net zero ready," often using made-in-B.C. technology.

In the building sector, Budget 2022 continues to make clean, electric heat pumps and home and building energy-efficiency improvements more affordable for people and businesses through $43 million for the CleanBC Better Homes, Better Buildings program. It also removes the PST on purchases of heat pumps and provides additional incentives for people living in rural and northern regions. These changes will come into effect April 1, 2022.

Additional supportive funding has been committed through BC Hydro’s electrification plan, which will make it easier for people and businesses to switch from fossil fuels to made-in-B.C. clean electricity.

Budget 2022 also ensures that B.C.’s clean transition remains affordable for all British Columbians. With $120 million in funding to continue the Climate Action Tax Credit, Budget 2022 is offsetting the impact of carbon taxes to low- and moderate-income individuals and families.

CleanBC funding totals are in addition to climate-related spending on energy efficiency for public-sector buildings, the First Nations Clean Energy Business Fund and the Innovative Clean Energy Fund.

Budget 2022 makes the choices needed to build a stronger B.C. by investing in the province’s economic, environmental and social strength to make life healthier and more affordable for people now and in the years ahead.

Quotes:

Selina Robinson, Minister of Finance–

“Recent climate-related disasters have tested the people of British Columbia and reinforced the need for collective action to secure a low-carbon future. Budget 2022 makes strong investments to help us fight climate change, and makes it easier and more affordable for people, communities and industries to make climate-smart decisions.”

George Heyman, Minister of Environment and Climate Change Strategy –

“Budget 2022 is tackling the climate emergency head on with record investments in our CleanBC Roadmap to 2030. This critical funding backs our climate commitments with over $1.2 billion in new funding to build a B.C.-led clean economy that makes life better for people. It means substantial new investments to reduce emissions and remove pollution from our environment, new funding for electric vehicles, a cleaner industry, more local government climate action and cleaner buildings. We’re working hard to fight the climate crisis, build back better from recent extreme weather and make sure people and communities across B.C. are ready for the challenges and opportunities ahead.”

Bruce Ralston, Minister of Energy, Mines and Low Carbon Innovation –

“With a strong foundation of existing programs and supports through CleanBC, funding from Budget 2022 ensures that we can continue to build on work that we have already accomplished. The transition to a low-carbon economy remains one of our top priorities, while making cleaner choices more affordable for British Columbians.”

Nathan Cullen, Minister of Municipal Affairs –

“Local governments are on the leading edge of fighting climate change and our government is committed to amplifying their work. Budget 2022 provides $76 million in new funding to create a new climate-action program that will support local governments in developing more resilient, compact and environmentally sustainable communities.”

The Bank of Russia acted quickly to shield the nation’s $1.5 trillion economy from sweeping sanctions that hit key banks, pushed the ruble to a record low and left President Vladimir Putin unable to access much of his war chest of more than $640 billion.

The central bank more than doubled its key interest rate to 20%, the highest in almost two decades, and imposed some controls on the flow of capital. It was part of a barrage of announcements that eventually restored some calm after a rout that pushed some Russian Eurobonds into distressed territory last week.

“The Bank of Russia will be very flexible in using all necessary instruments,” Governor Elvira Nabiullina said in brief televised remarks in Moscow.

Facing the risk of a bank run, a rapid sell-off in assets and the steepest depreciation in the ruble since 1998, policy makers banned brokers from selling securities held by foreigners starting Monday on the Moscow Exchange. Exporters were ordered to start mandatory hard-currency revenue sales and stock trading was temporarily suspended in Moscow.

“The ruble has ceased to be a freely convertible currency with the sweeping sanctions,” said Friedrich Heinemann, head of the corporate taxation and public finance department at German think thank ZEW. “In terms of currency policy, this throws Russia back to the early 1990s and the time before the country’s comprehensive economic opening.”

Less than a week after Putin ordered his military to invade Ukraine, Russia is at risk of succumbing to the biggest financial crisis of his more than two decades in power. He gathered Nabiullina and other top officials in the Kremlin to discuss plans for a response, calling the U.S. and its allies who joined in the sanctions “the empire of lies.”

The steps taken so far on Monday represent the most forceful measures by Russia after the latest round of sanctions, with the U.S. and the European Union agreeing to block access to much of the $640 billion the country’s central bank has built up as a buffer to protect the economy.

Additional measures taken by global governments to exclude some Russian banks from the SWIFT messaging system could further choke up the country’s banking system. Sanctioned institutions dominate Russia’s financial sector with $1 trillion in assets.

But the U.S. and Europe remain reluctant for now to sanction Russian energy, seeking to insulate the world economy from a greater shock. Germany’s Economy Ministry said on Monday that purchases of Russian gas remain possible using SWIFT even after the latest curbs.

In the absence of even wider trade sanctions that could ensnare Russian energy shipments, the policies implemented so far may be enough to stabilize markets, according to Renaissance Capital. The ruble recouped some losses and was trading nearly 14% weaker at around 96 per dollar as of 4:26 p.m. in Moscow. It was briefly down more than 30% earlier in the day.

“All these measures should limit the depreciation of the ruble,” said Sofya Donets, economist at Renaissance Capital in Moscow. “If the run on FX continues, we would anticipate additional direct restrictions on domestic operations.”

Nabiullina, who took no questions from reporters on Monday, said the central bank didn’t intervene in the currency market on Monday as a result of the limitations on its reserves. It spent $1 billion last Thursday and a smaller amount the following day to shore up the ruble, she said.

“We will make further decisions on monetary policy based on how the actual situation develops while assessing risks primarily in terms of the external conditions,” Nabiullina said.

Decisions to suspend some regulatory requirements amounted to a capital boost for banks by the equivalent of 900 billion rubles ($8.6 billion), she said.

The ruble’s 24% drop so far this year is the worst slump globally, prices compiled by Bloomberg show. At current levels the ruble’s slump is the biggest since 1998, the year the nation’s economy went into a tailspin and the government defaulted on its local debt.

S&P Global Ratings lowered Russia’s credit score below investment grade on Friday, while Moody’s Investors Service — which rates Russia one notch above junk — put the nation on review for a downgrade.

Policy makers are counting that the steep rate hike, alongside the mandatory conversion of export revenues and a halt to outflows from the financial market, will help restore confidence and minimize losses at home even as war continues to rage across the border.

“This is merely a reaction by the central bank to the fact that sanctions have weakened, completely neutralized their defense arsenal that they’ve built up in the past five to 10 years,” said Simon Harvey, head of FX analysis at Monex Europe Ltd. “It’s unprecedented escalation and markets are very poorly positioned for it.”

Russians were already lining up at cash machines around the country as demand for foreign currency soared. The central bank has said it was increasing supplies to ATMs to meet need and issued another statement Sunday vowing to provide banks “uninterrupted” supplies of rubles.

Most of Europe has closed its airspace to Russian carriers, which could make it difficult to physically transport cash into the country.

“I think rubles will be plenty, the question is FX,” said Viktor Szabo, an investor at Aberdeen Asset Management Plc. in London. “With reserves partially blocked, the central bank will have to prioritize, and I guess population will not be on top of the list.”

Oil and gas revenue remains a lifeline as the sale and transport of energy have largely escaped disruptions. At current prices, Russia was running a monthly current-account surplus of about $20 billion.

Still, damage to the economy will be severe from the combination of wild swings in the exchange rate and the soaring cost of money. Bloomberg Economics was already predicting a contraction in the first and second quarter even before the weekend’s sanctions and now sees the risk of an even “deeper downturn.”

Renaissance Capital said it now expects a recession this year, compared to a forecast of 3% growth expected as recently as last week.

The continued flow of oil will likely provide some relief, given the World Bank calculates commodities account for almost 70% of goods exports. About 43% of the country’s crude and condensate output is sold abroad.

If crude prices stay around $90 this year, the country’s budget could get more than $65 billion in extra revenue, adding to the Kremlin’s financial strength, economists said recently. Oil at $100 would boost the windfall closer to $73 billion.

In Russia, memories linger of hyperinflation that peaked at more than 2,500 percent in 1992 and wiped out savings in the wake of the Soviet collapse. Price growth is already running at more than double the central bank’s target, despite a series of rate hikes since last March.

Renaissance Capital estimates the suspension of operations with non-residents alone could prevent $50 billion in possible capital outflows in the coming weeks. The freeze on such transactions may stay in place for long, according to RenCap’s Donets.

“These measures may help calm down the increased market nervousness, but at the same time they undermine the foundation of monetary policy, which is focused on inflation targeting and a flexible exchange rate,” said Natalia Lavrova, chief economist at BCS Financial Group in Moscow. “We do not rule out a possible rate hike going forward or further unexpected and non-market decisions.”

(Updates with governor’s comments starting in third paragraph.)

(Bloomberg) -- Turkey’s economy expanded faster than peers in the fourth quarter as interest-rate cuts spurred a recovery from the pandemic, but the subsequent rise in the inflation rate could dent growth this year.

Gross domestic product rose 9.1% in the October-to-December period from a year earlier, bringing the full-year expansion to 11%. The quarterly growth beat the median estimate of 9% in a Bloomberg survey, and the annual figure is the highest among G-20 nations.

The expansion was driven by a surge in exports amid a recovery in key export markets in Europe. Domestic consumption was another key driver although there were signs consumer confidence was hurt during the final weeks of the year, when President Recep Tayyip Erdogan’s push for lower interest rates resulted in a currency crisis.

The lira’s massive drop -- it had lost as much as half its value within a few weeks before the government intervened -- has fueled inflation to around 50%, eating into consumers’ disposable income. Russia’s invasion of Ukraine is expected to further add to inflationary pressures, clouding the outlook for growth this year.

“Turkey’s economy faces the risk of another shock from rapidly rising energy and agricultural commodity prices caused by Russia’s war in Ukraine, which also weighs on the lira,” said Piotr Matys, an analyst at InTouch Capital Markets Ltd. “Inflation is likely to stay high for longer reducing disposable income of Turkish households while corporates will struggle to absorb consistent inflationary pressure from imported commodities.”

Inflation Outlook

Under pressure from the president, the central bank cut interest rates by 500 basis points in four consecutive moves from September to the end of 2021. While the cuts led to an uptick in spending and lira depreciation saw exporters contribute more to overall growth, price gains accelerated to their highest in two decades.

Consumer confidence hovered around historic lows in the first quarter as a result. Household consumption, which accounts more than a half of the economy, rose 21.4% during the first quarter of 2021 from a year earlier. Exports rose 20.7% during the same period.

Oil price surge from Russia’s war on Ukraine will likely add to inflationary pressures and may result in a decline in the number of foreign visitors from those two countries. They accounted for more than a quarter foreign tourists last year.

“A high annual growth can be expected again in the first quarter of 2022,” but a decline thereafter will likely bring the overall annual growth toward 4%,” said Enver Erkan, chief economist at Tera Yatirim.

The government’s official target is 5% and the International Monetary Fund’s estimate is 3.3%.

Coming Up

Turkey’s Statistical Institute will publish February inflation data on March 3. The central bank’s next rate-setting meeting is scheduled for March 17.

Global management consultancy AlixPartners has surveyed more than 3,000 CEOs and executive globally to gain insights in the key trends and priorities in the boardroom. The report concludes that business disruption across the business landscape has reached unprecedented heights, with four major forces that will longer term transform the world economy.

Demographic decline

For large parts of the world, the decade of the 2020s marks a stark transition: It is the first decade in which all of the leading economies across the globe – Europe, the US, Japan, and China – will see labor force growth markedly slow and, in many cases, shrink.

Retirements will outpace new workforce entrants in almost every major economy. Indeed, only India, Africa and parts of the Middle East will see meaningful labor force growth in this decade. This will present a major economic tailwind: Fully a third of GDP gains over the last six decades have come directly from labor force growth.

of the CEOs surveyed, four in five (80%) told AlixPartners they fear the current labor shortages may be permanent.

Technological acceleration

The explosion in new technologies is both a boon and a bane – technological innovation will become the principal driver of economic growth and promises to improve our lives and our world, but it is also the primary source of disruption and dislocation.

This is the tsunami wave that has executives most worried. The 2020s are seeing the emergence of the so-called bionic enterprise: the merging of human capital with artificial intelligence, big data, robotics, and an array of digital technologies to drive nextorder business outcomes. The mission for companies is clear: Be digital or die.

Climate transition

The effects and urgency of climate change have become increasingly apparent and accepted. And it is not just the long-term effects, but also the growing climate volatility as we see a marked increase in extreme weather events, both devastating and costly.

As important as climate change itself is our response to it. Roughly $2 trillion annually is now being invested in new renewable energy technologies, and fully 50% of investment dollars are now tied to net zero emissions requirements. Moreover, ESG demands from a broad range of stakeholders – including customers, employees, investors, and regulators – are driving companies to set more ambitious goals.

We should expect to see a plethora of new technologies and operating models aimed to drive a more sustainable set of environmental outcomes.

Deglobalization

After nearly three decades of expansion, the forces of globalization – which have helped fuel economic growth through greater trade, exchange, and openness – are in retreat. Barriers are going up, and global trade declining. Protectionism is on the rise.

The world’s two largest economies, the US and China, appear to be on a path of continued confrontation. Actions like Brexit and punitive trade wars are making economies more isolated than not.

A long-term realignment of supply chains is underway. The biggest near-term implication will be increased economic friction, reversing more than two decades of falling prices and access to cheap goods. We should expect continued rising prices and inflation, as well as the distinct possibility of increased global conflict.

Commenting on the four mega trends, the CEO of AlixPartners Simon Freakley said: “The pandemic presented businesses and their leaders with the most acute set of disruptors since World War II. However, CEOs view these issues as paling in comparison to the demographic, technological, climate, and international trade challenges that their businesses must confront today and in the years ahead.”

(Bloomberg) — Global governments remain reluctant for now to sanction Russian energy, seeking to insulate the world economy from a greater shock even as they tighten the financial grip on the country following its invasion of Ukraine.

While oil last week briefly passed $100 a barrel for the first time since 2014 and European natural gas prices jumped as much as 62%, the gains were partly reversed as the U.S. and European nations avoided sanctioning Moscow’s massive energy supplies for punishment.

Advertisement

Article content

They continue to resist doing so despite fresh plans to further annex President Vladimir Putin’s economy from the international monetary system. Although some Russian banks will now be excluded from the SWIFT payment messaging system, one official said the White House is looking at exemptions for transactions involving the energy sector.

The current reluctance to crack down on the source of much of Russia’s wealth reflects the fear that doing so would send energy prices surging even higher, transmitting a stagflationary mix of faster inflation and slower growth around an already fragile world economy.

The reprieve may support Putin’s under-threat economy, where commodities account for more than 10% of activity and much of the nation’s budget.

Advertisement

Article content

“Financial sanctions are often there as a signal of disapproval rather than a real attempt to cause pain and damage,” said John Gieve, a former U.K. government official and central banker. “Arguably that is the case now. We are not restricting energy exports because that would mean more pain for us than we are willing to bear.”

The avoidance of targeting Russian energy still may fade the longer the conflict rages and the more countries utilize alternative energy supplies. British Foreign Secretary Liz Truss said Saturday that the U.K. would support restricting Russian energy exports to Europe and that the U.K. was working with Group of Seven partners to reduce dependency on Russia.

Separately, BP Plc moved to dump its shares in oil giant Rosneft PJSC, taking a financial hit of as much as $25 billion by joining the campaign to isolate Russia’s economy.

Advertisement

Article content

Russia is a commodities-powerhouse, producing more than 10% of the world’s oil and natural gas, with Europe reliant on it for a third of its gas.

“Energy sanctions are certainly on the table,” White House Press Secretary Jen Psaki said on ABC’s “This Week” on Sunday. “We have not taken those off, but we also want to do that and make sure we’re minimizing the impact on the global marketplace and do it in a united way.”

The invasion-driven surge in energy prices already has economists predicting a higher and delayed peak in inflation as well as a hit to growth as consumers and companies are forced to allocate more of their budgets to fuel and heating.

Even with Russian energy being left alone, the war’s first few days have shown there’ll likely be snags maintaining a smooth flow of oil. Many buyers have backed away from buying Russian crude cargoes for fear of getting ensnared in sanctions or damaging their reputation. Urals, Russia’s most important export grade, is trading at a record discount to international benchmarks.

Advertisement

Article content

Many banks in Europe and China also have backed away from financing Russian commodity deals, at least in the short term, and tanker owners are reluctant to take on the risks of loading at Russian ports.

“Even if it is possible to pay counter-parties under trade contracts, payments will be in stupor in the near future due to exchange-rate volatility,” said Sofya Donets, economist at Renaissance Capital in Moscow. “For a period of uncertainty, trade will be made with great difficulty.”

But the fallout would be much worse if curbs were imposed on Russia.

The latest limits on finance are a “welcome move but insignificant to cut oil and gas flows,” said Thierry Bros, a professor at the Paris Institute of Political Studies. “We will still be in a position to pay for gas.”

Advertisement

Article content

In a scenario in which Europe’s gas supply was cut off, the euro-area would tumble into recession, according to Bloomberg Economics. The U.S. would suffer significantly tighter financial conditions and growth would diminish, leaving the Federal Reserve potentially having to raise interest rates in a slowing economy, the economists wrote last week.

At JPMorgan Chase & Co., economists led by Bruce Kasman estimate that a sustained shutting-off of Russian oil exports could propel the price of crude to $150 a barrel, potentially lowering global growth by 3 percentage points and raising inflation by 4 percentage points.

Still, Kasman’s team noted a nuclear agreement with Iran and the release of oil from the U.S.’s strategic reserve could offset as much as two-thirds of the shortfall from the cessation of Russian oil shipments.

Advertisement

Article content

Other ways of opening room to bash Russia and mitigate the aftershock include reviving coal-fired power stations and encouraging governments, including China’s, to tap their own reserves in a coordinated fashion.

As for Russia, the continued flowing of oil will likely provide some relief given the World Bank calculates commodities account for almost 70% of goods exports. About 43% of the country’s crude and condensate output is sold abroad.

The central bank’s latest projections showed the economy could grow 2%-3% this year, down from 4.7% in 2021. Inflation, though, is running at more than double its target, despite 525 basis points in interest-rate hikes since last March.

If crude prices stay around $90 this year, the country’s budget could get more than $65 billion in extra revenue, adding to the Kremlin’s financial strength, economists said recently. Oil at $100 would boost the windfall closer to $73 billion.

At Natixis SA, economist Alicia Garcia Herrero said sanctions on energy could still be in the cards.

“The West is finding ways to reduce the impact of a commercial embargo, which would include energy, but it has not found it yet,” Garcia Herrero said. “However, it is a question of time.”

London (CNN Business)Vladimir Putin has been expecting the West.

Since 2014, when the United States and its Western allies imposed sanctions on Moscow following the annexation of Crimea and the downing of Malaysian Airlines Flight 17, Russia's president has been trying to build an economy capable of withstanding much tougher penalties.

The West this week announced several rounds of sanctions after Russian troops invaded Ukraine. The penalties target the heart of the Russian financial system and will put the country's "fortress economy" to the test.

The latest barrage came Saturday, when the United States, the European Union, the United Kingdom and Canada said they would expel some Russian banks from SWIFT, a global financial messaging service, and "paralyze" the assets of Russia's central bank.

Fear of what sanctions might do sent Russian stocks crashing 33% on Thursday. They have since recovered some of those losses, but the ruble continues to trade near record lows against the dollar and the euro. Russian markets will likely come under renewed pressure when trading resumes Monday.

Russia's $1.5 trillion economy is the world's 11th biggest, just behind South Korea, according to World Bank data. Since 2014, its gross domestic product has barely grown and its people have gotten poorer. The value of the ruble has also tumbled, shrinking the value of the Russian economy by $800 billion.

Over the same period, Moscow has tried to wean its oil-dependent economy off the dollar, limited government spending and stockpiled foreign currencies.

Putin's economic planners have sought to boost domestic production of certain goods by blocking equivalent products from abroad. Moscow has meanwhile amassed a war chest of $630 billion in international reserves — a huge sum compared to most other countries.

David Lubin, a Citi economist and associate fellow at Chatham House, said "fortress economics" requires the creation of big foreign currency reserves that can be spent if sanctions bite.

"Russia has followed this pattern assiduously," he wrote recently.

Some of those reserves are already being deployed. The Russian central bank said Thursday it was intervening in the currency markets to prop up the ruble. And on Friday, it said it was increasing the supply of bills to ATMs to meet increased demand for cash. Russian state news agency TASS reported that several banks had seen increased withdrawals since the invasion of Ukraine, notably of foreign currency.

While building up a war chest, Putin's austere strategy has also limited economic growth, investment and productivity, and prioritized state companies over private business. The incomes of ordinary Russians have regressed to levels last seen in the early 2010s, and new foreign direct investment is minimal. Russia has also failed to diversify away from oil and gas, leaving it heavily exposed to swings in global commodity prices.

Taking on the 'fortress'

After Russian troops attacked Ukraine from the north, south and east, US President Joe Biden on Thursday unveiled sanctions designed to damage Russia's economy and turn Putin into an international "pariah."

The US penalties target Russia's two largest financial institutions, Sberbank and VTB, and prevent them from processing payments through the US financial system. Russian state-owned companies will not be allowed to raise capital through US markets. The sanctions cover nearly 80% of banking assets in Russia.

The United States is also trying to hobble Russian military and industrial companies by preventing them from buying critical technology such as advanced computer chips.

The European Union, the United Kingdom, Japan, Australia and other countries announced sanctions of their own against Russian companies and individuals, coordinated action that is unprecedented in terms of its scope and potential economic impact. US, UK and EU officials went further on Friday and sanctioned Putin himself.

The West tightened the screw again on Saturday. The United States, the European Union, the United Kingdom and Canada said in a joint statement that they would remove some Russian banks from SWIFT, a high security messaging network that connects thousands of financial institutions around the world.

"We are engaging with European authorities to understand the details of the entities that will be subject to the new measures and we are preparing to comply upon legal instruction," SWIFT, which is based in Belgium, said in a statement.

The Western coalition said it would also take steps to prevent Russia's central bank from deploying its international reserves to shore up the ruble. Ursula von der Leyen, president of the European Commission, said in a statement that the measures would "paralyze the assets of Russia's central bank."

Saturday's announcement came as Russian troops attacked cities across Ukraine and was thin on detail. The West did not say which Russian banks would be removed from SWIFT, nor how it would target the central bank.

But a senior Biden administration official told reporters the measures would show that "Russia's supposed sanctions-proofing of its economy is a myth."

"The $600 billion-plus war chest of Russia's foreign reserves is only powerful if Putin can use it, and without being able to buy the ruble from Western financial institutions, for example, Putin's central bank will lose the ability to offset the impact of our sanctions," the official said.

The sanctions package is unprecedented in scale, even before the measures announced Saturday.

"I don't think we have seen anything like this, and it's much, much more severe than sanctions in 2014," Iikka Korhonen, the head of the Bank of Finland Institute for Emerging Economies and an expert on Russia's banking and financial systems, told CNN Business on Friday.

Still, Russia has been preparing its economy for this moment, and global oil prices of $100 per barrel are producing huge amounts of revenue for the state.

"They can manage for a while," said Korhonen. "But the longer this lasts, it means the growth will be slower."

Balancing act

Western countries have sought to punish Moscow for the invasion without doing major damage to their own economies. Natural gas prices are extremely high in Europe, and cutting off supplies from Russia could drive them higher. Reduced exports of Russian crude would similarly hike oil and gasoline prices.

SWIFT is seen as a particularly blunt instrument.

Removing Russia entirely from SWIFT would make it much harder for financial institutions to send money in or out of the country, delivering a sudden shock to Russian companies and their foreign customers — especially buyers of oil and gas exports denominated in US dollars.

But targeting only certain Russian banks could allow payments to be made in exchange for Russian oil and gas exports.

With Russian troops advancing on the capital Kyiv, some say the West should be willing to pay a steep economic price.

"We don't have five years to slowly degrade the Russian economy. We need to do it now," said Tyler Kustra, an assistant professor of politics and international relations at the University of Nottingham in England.

— Nathan Hodge and Vasco Cotovio contributed reporting.

Growth is the gambit for the Liberals as tax hikes are out and spending cuts won’t happen.iStock/The Globe and Mail

Ottawa has gone all in on its bet that the economy can outpace the enormous debt burden incurred during the COVID-19 pandemic. Tax hikes are out, spending cuts won’t happen. Growth is the gambit.

“Above all, we know that our national focus, once we emerge from COVID-19, must be growth and competitiveness,” Finance Minister Chrystia Freeland asserted in her economic and fiscal update in December. “Measures to promote them will figure prominently in the budget.”

The Liberals have pointed to the country’s sizzling labour market as proof of their economic management prowess. Canada is indeed a leader among developed countries in creating jobs. But we’re at the back of the pack in creating wealth.

Rising productivity, not jobs, is what will be key to not just outrunning the shadow of the federal debt burden, but in creating the fiscal capacity to deal with climate change, an aging population and a host of other huge challenges in coming decades.

Ms. Freeland’s fiscal update speech mentioned jobs nine times. Productivity got zero mentions. Competitiveness, just one.

That lopsided emphasis is one warning sign. Another is Canada’s last-place finish in an October study from the Organization for Economic Co-operation and Development on projected growth in per capita gross domestic product from 2020 to 2060 among its 38 member countries. That’s in keeping with a dismal long-term trend that has seen Canadian productivity growth slide over the past 50 years.

If the Liberals’ gambit is to pay off, that 50-year slump must end. Canada needs a productivity plan. But so far, the federal government hasn’t produced one. “There’s a lack of ambition, a lack of commitment,” says Scotiabank chief economist Jean-François Perreault.

There were some micromeasures in the budget aimed at boosting the rate of technology adoption by small and medium-sized companies. Ms. Freeland has pointed to “social infrastructure” spending as the foundation for the Liberals’ growth agenda, including more money for education, housing and higher levels of immigration. The biggest single initiative is child-care expansion, which the government portrays as a catalyst for productivity comparable to continental free trade, asserting it will boost economic growth for decades.

But economists cast cold water on those assertions, particularly the notion of a long-lived effect. There will be some boost from smoothing the path to the labour market for parents, although for the most part that will come from the hard, slow work of increasing the number of child-care spaces rather than the higher-profile policy of slashing the fees parents pay.

But even child care, by far the most ambitious policy the Liberals have presented, falls far short of what’s needed to reverse Canada’s decades-long slide in productivity and wealth creation. Big ideas are needed to galvanize growth, to set Canada on a path to greater prosperity.

The big slump

Canada real GDP per capita growth, quarterly, 1961-2020

the globe and mail, source: scotiabank Economics;

Statistics Canada

The big slump

Canada real GDP per capita growth, quarterly, 1961-2020

the globe and mail, source: scotiabank Economics;

Statistics Canada

The big slump

Canada real GDP per capita growth, quarterly, 1961-2020

the globe and mail, source: scotiabank Economics; Statistics Canada

“We need a strategy now,” says Perrin Beatty, president and chief executive officer of the Canadian Chamber of Commerce, arguing that the federal government needs to move quickly and not wait until the coronavirus crisis has receded.

Ahead of the 2022 federal budget, The Globe talked to economic thinkers across the country about what they view as key parts of a growth agenda for Canada – and to stick to ideas the federal Liberals could conceivably sign on to.

Hang your hat on a goal

John F. Kennedy didn’t just say America would land astronauts on the moon. In 1962, the then U.S. president declared America would do it before the end of the 1960s, committing to a firm and ambitious goal even though not every part of a plan had been worked out. (Indeed, his landmark speech on the space race noted that American spacecraft would use new alloys, “some of which have not yet been invented.”)

By contrast, Ottawa has committed to boosting Canada’s productivity in only the vaguest terms, verging on wishful thinking. A chart in last spring’s budget purported to show long-term productivity gains resulting from child care and other measures. But its projections simply assumed a surge in productivity, and a reversal of a half-century of decline.

“We need an objective-based economic agenda,” says Mr. Perreault, suggesting that the government explicitly commit to a goal of boosting GDP per capita by 2 per cent a year. That might not seem impressive, but it would mean a doubling of current rates.

The target could be to get Canada into the top 10 among OECD countries for productivity growth within a decade. Or, as Mr. Beatty suggests, there could be a goal such as a certain percentage of trade from Asia flowing through Canadian ports.

Whatever that goal is, it shouldn’t be easy, he says. For there to be a prospect of success, there also needs to be the possibility of failure – and a motivation for action by the government. The federal Liberals are well aware of the power of such a public commitment; it is at the heart of their climate change plan.

Canada bringing up the rear

Projected real GDP per capita growth, CAGR*,

OECD countries, 2020-2030, %

Costa Rica

Czech Rep.

New Zealand

OECD average

Euro area avg.

*Compound annual growth rate

the globe and mail, Source: business council

of british columbia; oecd

Canada bringing up the rear

Projected real GDP per capita growth, CAGR*,

OECD countries, 2020-2030, %

Costa Rica

Czech Rep.

New Zealand

OECD average

Euro area avg.

*Compound annual growth rate

the globe and mail, Source: business council

of british columbia; oecd

Canada bringing up the rear

Projected real GDP per capita growth, CAGR*, OECD countries, 2020-2030, %

Costa Rica

Czech Rep.

New Zealand

OECD average

Euro area avg.

*Compound annual growth rate

the globe and mail, Source: business council of british columbia; oecd

Bribe the provinces to create a national economic space

For decades, commissions and white papers have pointed to an obvious step Canada can take to accelerate growth: dismantle trade and regulatory barriers between provinces to create a unified national economic space. And for decades, those recommendations have collided with the political inertia of provinces unwilling to irritate their constituencies for the sake of the national good.

To cut through that made-in-Canada protectionism, Mr. Perreault suggests borrowing a page from the federal Liberals’ approach to health care (which is in provincial jurisdiction): Give the provinces money in exchange for dismantling those internal barriers.

He estimates that the federal government would reap a fiscal dividend of between $13-billion and $15-billion if there were free trade within Canada. Ottawa can offer that cash ahead of time to the provinces, a huge inducement to get on board with radical regulatory reform. “Basically, you’re bribing the provinces,” he says.

Create a pandemic buffer

The pandemic exposed an unlikely Achilles heel of the economy: Canada’s already overstretched intensive care capacity. Countries with higher per capita counts of ICU beds were more able to avoid, or at least minimize, lockdowns and other draconian measures, says David Macdonald, senior economist at the left-leaning Canadian Centre for Policy Alternatives (CCPA).

Provincial premiers are already clamouring for billions of dollars more in health care transfers. Mr. Macdonald suggests Ottawa accede to their requests, but tie that new funding, at least in part, to the provinces increasing spending on the infrastructure and staff needed to expand Canada’s ICU capacity – as a buffer against a future health emergency.

istock/The Globe and Mail

Cut red tape to go green

The federal Liberals want to shift the Canadian economy away from fossil fuels to a greener future, including battery production for electric vehicles. But Beata Caranci, Toronto-Dominion Bank’s chief economist and a senior vice-president, points out a major flaw in that push. A thicket of regulations means that it can take 15 years for a mine that would produce the minerals for batteries to start operating, an obvious disincentive for any investor, and particularly damaging for an emerging sector.

Clear out that thicket, Ms. Caranci says, with a goal of reducing the regulatory turnaround to just three years. That example echoes a broader point from others, that layers of regulations built up over decades are choking innovation. Dan Kelly, president and chief executive officer of the Canadian Federation of Independent Business, says the federal government needs to rethink about introducing any new regulations, at a minimum.

Even without a regulatory paring, Mr. Kelly says, Ottawa can move to reduce the (literal) paperwork burden on businesses by speeding a shift to virtual government – the virtues of virtual having been made clear during the pandemic.

Show-us-your-receipts corporate tax cuts

Cuts in the general corporate tax rate didn’t do much to spur investment over the past decade. And, in any case, the federal Liberals have not expressed any enthusiasm for a laissez-faire approach to business investment.

But there are glimmerings of a strategy to channel private-sector dollars toward boosting productivity. In 2018, the Liberals put in place targeted tax benefits for investment, with accelerated depreciation for certain sectors for investments made up until 2028.

Last year, the government introduced a measure to allow for the immediate expensing of eligible investments – but that program was limited to private Canadian-controlled corporations and only up to a ceiling of $1.5-million.

Mr. Macdonald says making accelerated depreciation a permanent measure could spur investment by the private sector, while avoiding the peril of cutting corporate tax rates only to see the resulting tax expenditures flow out of the company in the form of dividends or share buybacks.

Ms. Caranci of TD Bank has a variant of that idea: Give tax breaks to small and medium-sized companies based on their rate of expansion. That would challenge the political orthodoxy that has seen many federal and provincial governments lavish praise and tax benefits on small businesses. But those measures have also created a tax cliff, Ms. Caranci says, where businesses that expand see their tax rates climb sharply. A tax measure tied to growth would help to erode that tax cliff and reward businesses that dare to invest, expand and win, she says.

Streamline the tax code

The Income Tax Act has grown in heft and complexity since its introduction more than a century ago. But University of British Columbia economist Kevin Milligan proposes a reversal, if a gradual one, that would aim to continually simplify and consolidate rules and incentives in personal and corporate taxation. (Prof. Milligan, who was seconded to the Privy Council Office in fiscal 2020-21, says he does see the 2021 budget as laying out a strategy for rejuvenating economic growth.)

He says he’s wary of a big-bang approach to rewrite the tax code all at once. But a continuing commitment to eliminate a few complicated tax measures each year would, over time, create a more transparent system, he says. “That’s an agenda any government should want to grab onto.”

The government could pocket the revenue resulting from eliminating byzantine subsidies, or roll back tax rates, he says. The Liberals have already taken that latter approach in their first term, when they eliminated a slew of Conservative tax exemptions, then cut the middle income tax bracket for individuals.

Mr. Beatty makes a similar point, arguing that a wide-ranging review of the tax system is long overdue. But the goal should be to increase the efficiency and fairness of taxation, not necessarily to cut rates for businesses, he says.

istock/The Globe and Mail

Tap into grey power and parent power

Canada’s work force will need all hands on deck to avoid labour shortages as the population ages.

That imperative will include young seniors, and will require the federal government providing incentives for them to continue working past 65. A decade ago, the Conservatives tried to address that need with a move to gradually bump up the age of retirement – a policy the Trudeau Liberals promptly reversed after being elected in 2015.

A reversal of that reversal seems most unlikely. But Mr. Perreault of Scotiabank says there are other ways the Liberals could make delayed retirement more desirable, though not mandatory. One possibility: increasing the benefits from deferring Canada Pension Plan and Old Age Security benefits. Another would be to increase the amount that seniors can earn if they keep working, without reducing their government benefit payments.

Parents, particularly mothers, are another obvious cadre of reinforcements for a stretched work force. The Liberals are already moving on that front, with a child-care policy aimed at increasing work-force participation rates for women by cutting out-of-pocket fees for parents and by expanding capacity.

But the CCPA’s Mr. Macdonald suggests that further investment focus on capacity expansion will deliver a bigger impact on productivity than simply reducing fees for families already using child care.

Personnel trainer

There are tens of thousands of stay-at-home moms who desperately need training to re-enter the work force, says Wilfrid Laurier University economist Tammy Schirle. Yet formal training programs are typically tied to unemployment benefits, and are usually out of reach for women who have been out of the work force for years.

A new approach that untethered training from job loss and instead treated it as a bridge to employment, whatever the starting point, would not just benefit individuals, but eliminate mismatches and inefficiencies in the labour force, Prof. Schirle says.

Other people could also benefit: gig workers trapped in low-end jobs; labourers who will need a second, less physically demanding career as they age; and seniors. Ultimately, she says, a more efficient labour market is a key component of a more productive economy. “We’re looking for that efficient allocation of talent.”

Tilt the table on innovation

Former BlackBerry Ltd. chairman and co-CEO Jim Balsillie says he has a big idea to drive innovation that won’t cost Ottawa a dime: Stop giving away our best ideas, and corral that intellectual property within Canada. The tech entrepreneur and chair of the Council of Canadian Innovators says Canadian policy hasn’t kept up with seismic changes in the global economy, most notably the accelerating shift from a production economy to a knowledge economy.

For Mr. Balsillie, Ottawa’s current approaches, such as attempting to spur the growth of superclusters for key industries, simply fails to understand and embrace that change. The debate should not be about shifting from resource extraction to factories making gear for the green economy. Canada should not try to compete on labour costs in a world where many other nations can offer much more favourable terms.

Instead, the focus of policy should be creating conditions for Canadians to invent the next world-beating electric battery, rather than make someone else’s. “The money is owning the idea, and capturing value on that,” he says.

One immediate change he recommends: leverage federal research funding to capture more of the economic value of Canadian innovation. That could be done by requiring that the rights to any intellectual property have to be retained in Canada, so that domestic firms can make use of that technology.

istock/The Globe and Mail

Big data is another area that needs a public presence, says Mr. Balsillie, arguing that the federal government should create data collectives that can be licensed by private firms, rather than see big tech companies fill that void. Canada has a long tradition of using public institutions to build the country and economic capacity, he says. It’s time to build on that history.

Mr. Balsillie acknowledges that his proposals mark a necessary break with the prevailing mindset of official Ottawa, particularly the notion of abandoning a laissez-faire approach to intellectual property. But he says the stakes could not be higher. Canadians can either seize the high ground in the increasingly digitized global economy, and reap outsized benefits, or this country will see itself relegated to at best second-tier status.

The choice should be obvious for this government, or any other, Mr. Balsillie contends. “There is nothing partisan about prosperity.”

Your time is valuable. Have the Top Business Headlines newsletter conveniently delivered to your inbox in the morning or evening.Sign up today.

/cloudfront-us-east-2.images.arcpublishing.com/reuters/OFHTL6QD7JK2VBHMBWC7GZZHUQ.jpg)

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/tgam/SZF65VCN4ZF4HHGCLF2NBAQSYA.jpg)

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/tgam/FEUU5UQZBBD3JMC4CJT4HMDOM4.jpg)

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/tgam/GD6QYUBWSREU7ODNG45IP7GP4E.jpg)

:format(webp)/cloudfront-us-east-1.images.arcpublishing.com/tgam/O6RN6AS76NE4RELD7CJNGA5DAQ.jpg)