As the pandemic retreats and summer travel starts, hotels, airlines and rental car companies are expecting a big jump in business. Travelers also may have to prepare for longer lines, higher prices.

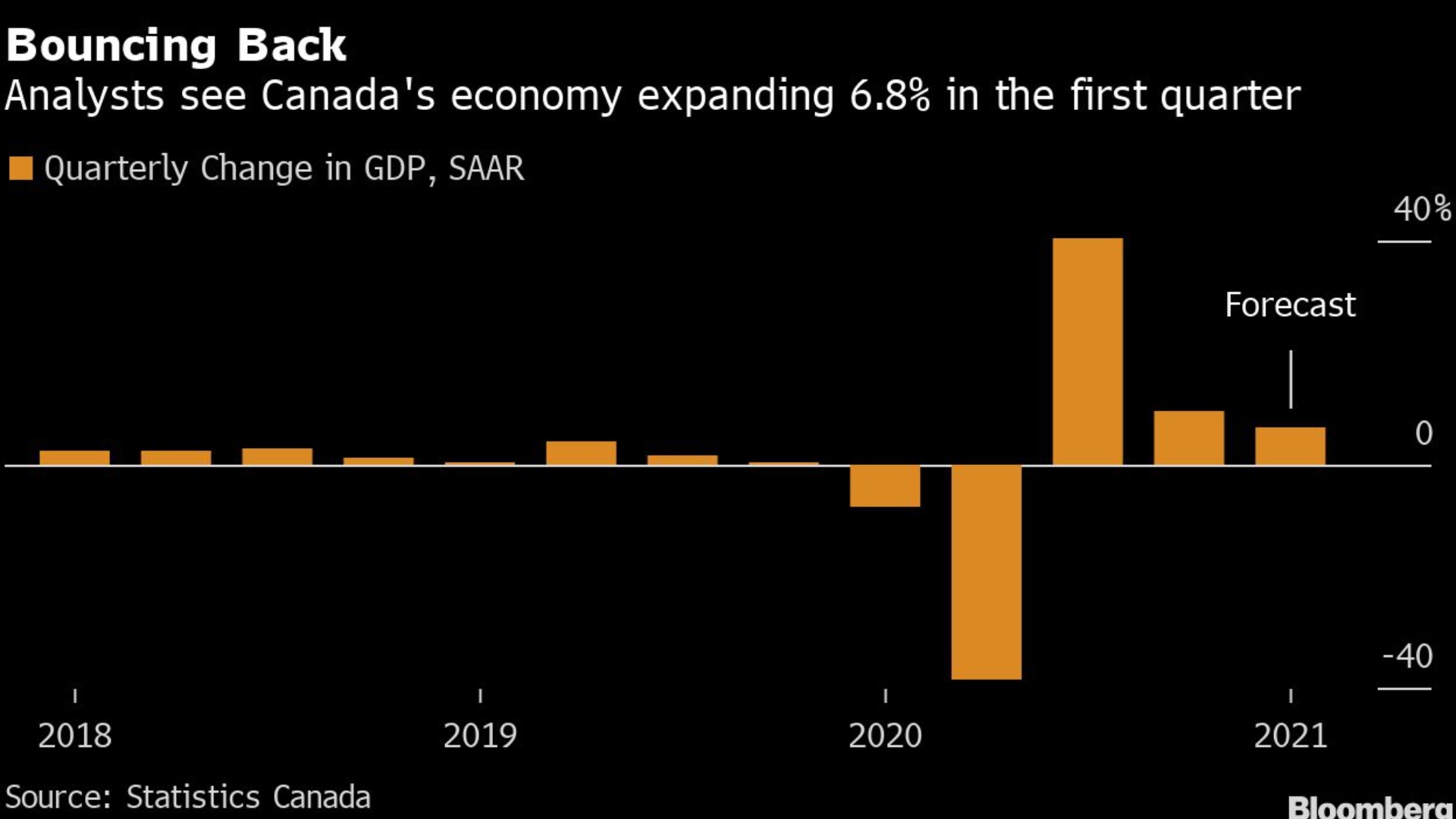

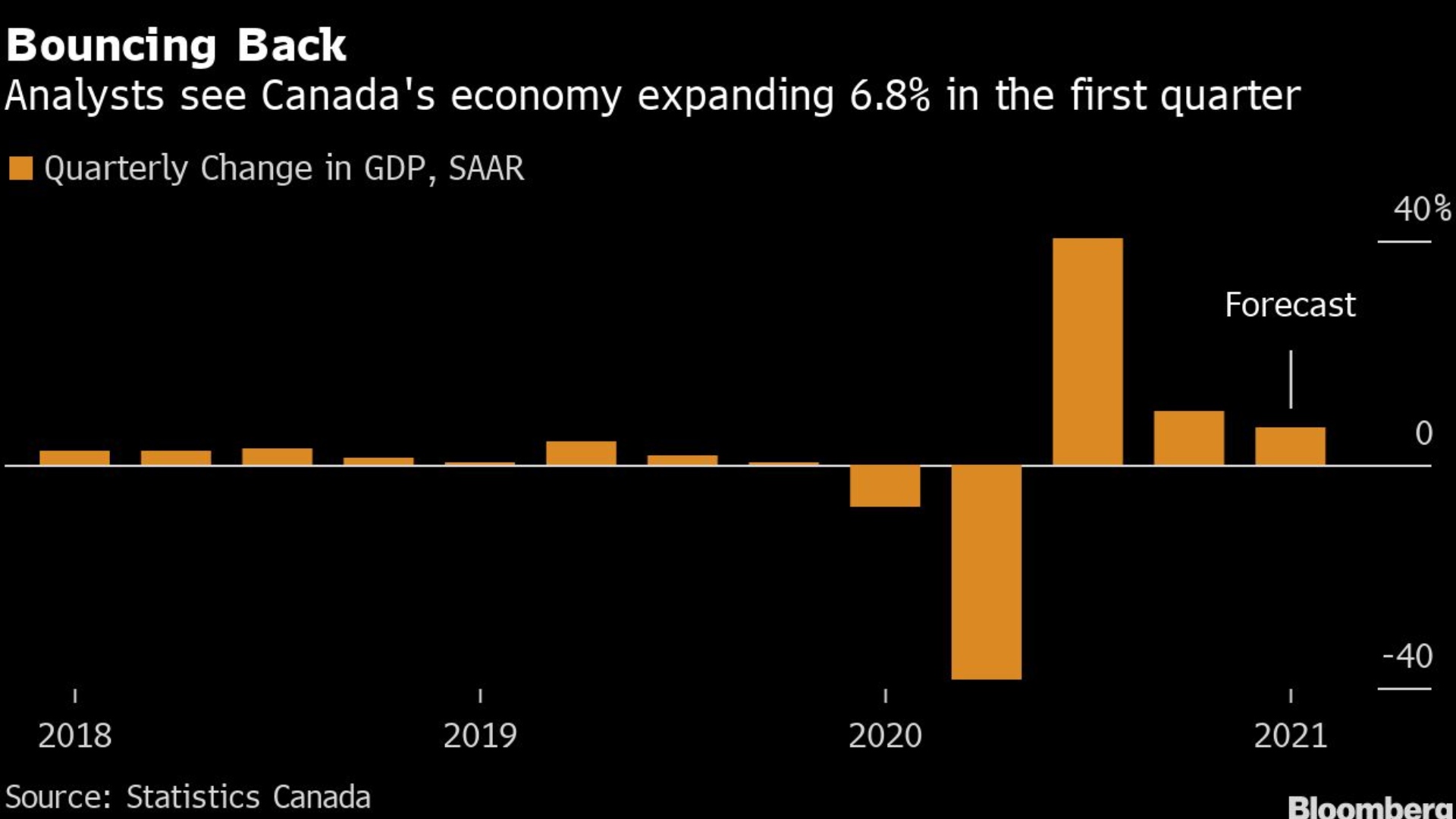

Canada’s economic recovery likely forged ahead in the first quarter, with a recovering export sector and red-hot housing market bringing total output to the cusp of its pre-pandemic level.

Statistics Canada is expected to report on Tuesday that gross domestic product expanded at an annualized pace of 6.8 per cent in the first three months of the year, according to a Bloomberg survey of 17 economists. That follows a 9.6 per cent gain in the fourth-quarter, and would bring production to within 1.6 per cent of where it was at the end of 2019.

While the expansion could slow down sharply in the second quarter amid a fresh wave of lockdowns, a strong report this week will stoke confidence in the country’s resilience to the containment measures. Economists are anticipating the pace of growth will return to above 6 per cent in the second half of 2021.

“The good news is as Covid restrictions seem to relax, the economy can bounce back quite quickly,” Royce Mendes, an economist at Canadian Imperial Bank of Commerce, said by phone.

One reason for optimism is that the economy has been recovering with little support from consumers, who have held off from spending over the winter months amid the restrictions to activity. Growth in consumer spending was probably flat in the first quarter, much as it was at the end of 2020.

That suggests pent-up demand could be building to drive outsize growth later in the year.

“The more interesting timing is the reopen period,” Beata Caranci, chief economist at Toronto-Dominion Bank, said by phone. “What does that normal look like for people? Does it unleash spending so that people start spending that excess savings?”

Growth Drivers

Exports and housing investment likely led the way at the start of 2021, along with businesses rebuilding inventories.

New home construction and real-estate sales rose to records at the start of 2021. Exports recorded solid gains, led by a strong rebound in aircraft production and some commodities. Restocking of inventories, meanwhile, was the main contribution to growth at the end of last year.

Adding to the tailwinds is an accelerating vaccination effort and continued government support, after Finance Minister Chrystia Freeland announced a new wave of spending in April.

The potential for a sharp rebound and a faster-than-expected full recovery is already prompting the Bank of Canada to start paring back its stimulus and warning of higher interest rates. Economists are anticipating a healthy 6.2 per cent expansion for all of 2021, only slightly behind a U.S. recovery projected at 6.5 per cent.

Signs indicate limited access to buildings in Toronto's financial district in March, after Ontario imposed new COVID-19 restrictions.

To be sure, it will be choppy and the second quarter could be very weak.

In April, provinces including Ontario, Quebec and British Columbia shut down parts of their economies to curb activity. The third wave of lockdowns has already led to fresh job losses, with employment falling 207,100 during the month. Retail sales, meanwhile, fell 5.1 per cent. That economic weakness is likely to extend in May.

Along with first-quarter data, Statistics Canada will release an early read on activity in April, which is likely to be negative.

“April’s GDP looks like a clunker,” Doug Porter, chief economist at Bank of Montreal, said by phone. “Every number we have for April has a red sign in front of it.”

But that could change quickly. About half of Canadians have now received a first shot of a vaccine and infections have declined in most of the country, raising the prospect of more reopenings in high-contact industries. Prime Minister Justin Trudeau’s government flagged a 75 per cent vaccination rate as a potential marker for looser restrictions, including at the Canadian border.

“Canada’s economy is expected to post some impressive bounce-backs in employment and retail trade in coming weeks,” Porter said in a report released on Friday.

(Bloomberg) -- Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

Turkey’s economy has continued to grow at a strong pace this year, an expansion that’s come at the expense of price and currency stability.

The economy outperformed all Group of 20 nations except for China in the first quarter after nearly stalling a year ago when the pandemic struck. It’s been bolstered by robust consumption on the back of last year’s government-led push to cut interest rates and boost lending.

Gross domestic product rose 7% from a year earlier and 1.7% from the fourth quarter. The median of 22 forecasts in a Bloomberg survey was for 6.3% growth compared to the same period in 2020.

Below are some of the highlights of the GDP report released by the state statistics institute in Ankara on Monday:

Household consumption -- estimated to account for about two-thirds of the economy -- continues to be one of the main drivers of growth. It jumped 7.4% from a year earlier.

The size of the economy grew to $728.5 billion in the first quarter from $717 billion in current prices last year.

Exports rose 3.3% on an annual basis. Imports dropped 1.1%.

Gross fixed capital formation, a measure of investment by businesses, rose an annual 11.4%. Government spending rose 1.3% after a 6.6% jump in the previous quarter.

The economy grew by 1.7% in the last quarter from the previous three months when adjusted for seasonality and the number of working days. Overall output rose 1.8% in 2020.

There is an “exchange rate illusion” in Turkey’s economic growth data, according to Enver Erkan, chief economist at Istanbul-based Tera Yatirim. Noting that the GDP per capita in U.S. dollar terms dropped nearly 40% since 2013 to around $7,700 last year, Erkan said Turkey’s recent economic model isn’t sustainable as the growth is mainly driven by consumption supported by government spending and loan campaigns.

“This comes at the expense of lira and price stability,” he said.

The government pushed banks to ramp up lending to help businesses and consumers ride out last year’s Covid-19 emergency. The credit boom was coupled with a front-loaded easing cycle. That growth push weakened the currency by 20% last year and kept headline inflation in double digits.

The currency losta further 10% against the dollar in the first quarter, especially after President Recep Tayyip Erdogan fired the central bank’s former hawkish governor Naci Agbal in March. The decision to fire Agbal, who had sought to restore the central bank’s credibility, set off a swift reversal of investor enthusiasm, sending Turkish markets into a nosedive.

There may be a limited drop in the pace of growth in the second quarter, according to Istanbul-based economist Haluk Burumcekci. “Uncertainties regarding the monetary policy makes it difficult to assess the upside risks on our growth expectation of 5.5% for 2021,” he said.

The data expose the challenge facing new central bank Governor Sahap Kavcioglu as he looks to restore price stability without cooling the economy ahead of the general elections in 2023.

Kavcioglu has pledged policy continuity after his appointment and kept benchmark interest rate unchanged at 19% for a second meeting this month, saying the pace of price gains had peaked in April. Consumer inflation quickened for a seventh month to 17.14% in April.

Canada’s economic recovery likely forged ahead in the first quarter, with a recovering export sector and red-hot housing market bringing total output to the cusp of its pre-pandemic level.

Statistics Canada is expected to report on Tuesday that gross domestic product expanded at an annualized pace of 6.8 per cent in the first three months of the year, according to a Bloomberg survey of 17 economists. That follows a 9.6 per cent gain in the fourth-quarter, and would bring production to within 1.6 per cent of where it was at the end of 2019.

While the expansion could slow down sharply in the second quarter amid a fresh wave of lockdowns, a strong report this week will stoke confidence in the country’s resilience to the containment measures. Economists are anticipating the pace of growth will return to above 6 per cent in the second half of 2021.

“The good news is as Covid restrictions seem to relax, the economy can bounce back quite quickly,” Royce Mendes, an economist at Canadian Imperial Bank of Commerce, said by phone.

One reason for optimism is that the economy has been recovering with little support from consumers, who have held off from spending over the winter months amid the restrictions to activity. Growth in consumer spending was probably flat in the first quarter, much as it was at the end of 2020.

That suggests pent-up demand could be building to drive outsize growth later in the year.

“The more interesting timing is the reopen period,” Beata Caranci, chief economist at Toronto-Dominion Bank, said by phone. “What does that normal look like for people? Does it unleash spending so that people start spending that excess savings?”

Growth Drivers

Exports and housing investment likely led the way at the start of 2021, along with businesses rebuilding inventories.

New home construction and real-estate sales rose to records at the start of 2021. Exports recorded solid gains, led by a strong rebound in aircraft production and some commodities. Restocking of inventories, meanwhile, was the main contribution to growth at the end of last year.

Adding to the tailwinds is an accelerating vaccination effort and continued government support, after Finance Minister Chrystia Freeland announced a new wave of spending in April.

The potential for a sharp rebound and a faster-than-expected full recovery is already prompting the Bank of Canada to start paring back its stimulus and warning of higher interest rates. Economists are anticipating a healthy 6.2 per cent expansion for all of 2021, only slightly behind a U.S. recovery projected at 6.5 per cent.

Signs indicate limited access to buildings in Toronto's financial district in March, after Ontario imposed new COVID-19 restrictions.

To be sure, it will be choppy and the second quarter could be very weak.

In April, provinces including Ontario, Quebec and British Columbia shut down parts of their economies to curb activity. The third wave of lockdowns has already led to fresh job losses, with employment falling 207,100 during the month. Retail sales, meanwhile, fell 5.1 per cent. That economic weakness is likely to extend in May.

Along with first-quarter data, Statistics Canada will release an early read on activity in April, which is likely to be negative.

“April’s GDP looks like a clunker,” Doug Porter, chief economist at Bank of Montreal, said by phone. “Every number we have for April has a red sign in front of it.”

But that could change quickly. About half of Canadians have now received a first shot of a vaccine and infections have declined in most of the country, raising the prospect of more reopenings in high-contact industries. Prime Minister Justin Trudeau’s government flagged a 75 per cent vaccination rate as a potential marker for looser restrictions, including at the Canadian border.

“Canada’s economy is expected to post some impressive bounce-backs in employment and retail trade in coming weeks,” Porter said in a report released on Friday.

The Paris-based think tank says it now expects the Canadian economy to grow by 6.1 per cent this year. The prediction is up from an estimate for growth of 4.7 per cent that the OECD made in March.

It says the rebound will be thanks to reduced COVID-19 restrictions in the second half of the year and external demand.

The OECD says growth in Canada for 2022 is forecasted at 3.8 per cent compared with a March estimate of four per cent.

Trending Stories

Could COVID-19 vaccine passports kick start Canadian economy?

Could COVID-19 vaccine passports kick start Canadian economy? – May 22, 2021

The improved outlook for Canada came as the OECD forecast global output would rise 5.8 per cent this year, up from its forecast of 4.8 per cent in December.

Statistics Canada is expected to release Canadian gross domestic product figures for the first quarter on Tuesday.

India’s gross domestic product grew 1.6 percent in the first quarter of 2021 compared with the same time last year, but that growth has been slowed by a surge in coronavirus infections.

India’s annual economic growth rate picked up in January-March compared with the previous three months, but economists are increasingly pessimistic about this quarter after a huge second wave of COVID-19 infections hit the country last month.

A slow vaccination drive and local restrictions after a massive second wave of infections and deaths across the country hit economic activities like retail, transport and construction while putting millions out of work.

India has recorded 28 million COVID-19 infections, second only to the United States, and 329,100 deaths as of Monday, although the rise has begun to slow.

The gross domestic product (GDP) grew 1.6 percent in January-March compared with the same period a year earlier, mainly driven by state spending and manufacturing sector growth, data from the statistics ministry showed on Monday.

Economists said the country faces a slowdown in consumer demand as household incomes and jobs have declined, with limited scope for the government to offer growth stimulus due to its rising debt.

Sakshi Gupta, a senior economist at HDFC Bank, said while the year-on-year numbers for the April-June quarter might look upbeat due to a low base, the sequential growth is likely to contract.

“With the spread of the virus more acute in rural areas in this wave, rural demand and sectors dependent on the rural economy might come under stress.”

Economists have cut their growth forecast for the fiscal year that began on April 1 to 8-10 percent from an earlier 11-12 percent.

Consumer spending – the main driver of the economy – rose 2.7 percent year-on-year in the January-March quarter following a revised 2.8 percent fall the previous quarter, data showed.

Annual growth of 6.9 percent in manufacturing and 14.5 percent in construction during the three months to March reflected signs of a recovery before the second wave hit the country.

Investments rose 10.9 percent compared with a growth of 2.6 percent the previous quarter, while state spending jumped 28.3 percent after almost no growth in the October-December period, data showed.

India also revised its annual GDP estimates for the fiscal year, predicting a 7.3 percent contraction, narrower than its earlier forecast for a downturn of 8 percent.

Slow vaccination

Prime Minister Narendra Modi has faced criticism for the slow pace of his four-month-old vaccination campaign, which has inoculated fewer than 4 percent of India’s 1.38 billion people.

The central bank, which has kept monetary policy loose while boosting liquidity to the economy, said last week the country’s growth prospects will depend on how fast India can arrest infections.

Analysts warn that the slow rollout could pose medium-term risks to growth, especially if the country were to experience a third wave of COVID-19.

Unemployment soared to a near one-year high of 14.7 percent in the week ending May 23, according to the Centre for Monitoring Indian Economy, a Mumbai-based private think-tank.

Krishnamurthy Subramanian, the chief economic adviser at the finance ministry, said some growth momentum had been lost after a surge in coronavirus cases.

“India continues to need monetary and fiscal policy support,” he said after the release of data.

It will take some countries three years to recover, warns OECD

Author of the article:

Bloomberg News

William Horobin

The OECD warned the problem of diverging fortunes could worsen further because of a failure to get enough vaccines and support to emerging and low-income economies.Photo by Getty Images

Article content

A strengthening world recovery from the COVID-19 pandemic risks leaving behind many regions, fuelling inequalities across and within borders, the Organization for Economic Cooperation and Development said Monday.

As the Paris-based group revised up its 2021 global growth forecast to 5.8 per cent from 5.6 per cent, it warned of gaping differences that mean living standards for some people won’t return to pre-crisis levels for an extended period.

In countries including Argentina and Spain, more than three years will elapse between the onset of the pandemic and a recovery of per-capita economic output, according to the new projections. That compares to just 18 months in the U.S. and under a year in China.

“It is with some relief that we can see the economic outlook brightening, but with some discomfort that it is doing so in a very uneven way,” OECD Chief Economist Laurence Boone said. “The risk that sufficient post-pandemic growth is not achieved or widely shared is elevated.”

Advertisement

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

The assessment sounds a note of caution as confidence surges in the world’s richest countries with the lifting of restrictions and the acceleration of vaccination campaigns.

The OECD praised governments for exceptionally swift and effective policy support that is now fuelling a rebound in trade, manufacturing and consumer spending. That will limit the scars the crisis leaves behind, the 38-member organization said.

But it warned the problem of diverging fortunes could worsen further because of a failure to get enough vaccines and support to emerging and low-income economies, which already have less capacity to absorb shocks and could face sovereign funding issues.

Without inoculations in all countries, the OECD said new variants and renewed lockdowns could hit confidence, plunge activity back into a disruptive stop-go pattern, and bankrupt firms.

“The rebound is pretty solid, pretty robust, but it depends crucially on whether we can keep up the rhythm of vaccination: it’s vaccination, vaccination, vaccination,” OECD Secretary General Angel Gurria said on Bloomberg Television. “The enemy is mutating, the enemy has variants, it’s changing its shape and its DNA and therefore we should not allow it, we should try to beat it as early as possible.”

Inflation Risk

The OECD also flagged a new threat of inflation due to higher operating costs, with virus containment and supply disruptions leading to shortages of components, and muted competition as a result of bankruptcies. Tensions should fade by the end of the year as production capacity normalizes and consumption shifts toward services.

Advertisement

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

“Inflation is expected to increase temporarily, but the longer-term outlook remains uncertain, with upside risks,” the OECD said. “A combination of possible negative supply-side effects could push up inflation by more than projected.”

There is also a risk that financial markets fail to look through the disruption. It called on central banks in advanced economies to maintain accommodative policy and allow temporary overshooting of their inflation goals.

“This is not the time to worry about inflation, although we should always keep it in the back of our minds,” Gurria said.

For governments, the OECD prescribed a combination of flexible fiscal support targeted particularly at small firms, and an effort to restore confidence with credible plans to repair public finances in the longer term. It also said public money should be spent swiftly on investment for a digital and lower-carbon economy.

“As countries transition toward better prospects, it would be dangerous to believe that governments are already doing enough to propel growth to a higher and better path,” Boone said.

Kevin Carmichael: Ruest says he's following 'business where business is going next' after sensing change in where winds are blowing on trade

Author of the article:

Kevin Carmichael

Canadian National Railway Co.’s chief executive, Jean-Jacques Ruest.Photo by National Post photo illustration

Article content

Executives are the most important economic actors, but that doesn’t automatically make them good stewards of the economy.

Consider the North American railroad industry and its obsession with the operating ratio, which measures operating expenses as a percentage of revenue. Canadian Pacific Railway Ltd. pushed its ratio all the way down to 54 per cent in the fourth quarter, setting it apart from its larger rival, Canadian National Railway Co., which had a ratio of about 61 per cent over the same period.

The former looks like the better company by that metric. Maybe it is. CP also has more cash and pays a higher dividend, both a per-share basis, than CN, according to data compiled by Canalyst, an analytics firm.

But the clear edge in growing the economy, and the company’s future prospects in the process, goes to CN, according to its chief executive, Jean-Jacques Ruest, who joined the Montreal-based company when it was privatized in 1996 and claimed the top job in the summer of 2018.

Advertisement

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

“We want to be a company that grows, and grows volume,” he said in an interview. “Our emphasis is on growing the bottom line by moving more freight.”

The distinction matters more than it did even a few months ago.

Earlier this month, Ruest snatched Kansas City, Mo.-based Kansas City Southern from CP chief executive Keith Creel by convincing KCS to accept his US$30-billion offer, even though it had already agreed to sell its assets to CN’s historic rival for US$25 billion in March.

Kansas City Southern (KSC) Railway locomotives idle on a fuel pad before pulling freight trains from Knoche Yard in Kansas City, Missouri.Photo by Luke Sharrett/Bloomberg files

But winning the prize won’t be as simple as outbidding a smaller rival. Analysts assume CN will have a tougher time with regulators who might disapprove of one of the bigger railways gobbling up a potential challenger. A combined CP and KCS would still have been the smallest of the Class I railways, but it would have been better positioned to challenge companies such as CSX Corp., Union Pacific Corp. and CN.

On the surface, Ruest’s bid will weaken competition. He needs a story about why that won’t hurt the economy and the narrative he’s chosen is a compelling one: a bigger CN, because of the company’s philosophy, means a bigger economy.

“Most of our benefit, to justify the investment, comes from growing the pie of the marketplace,” he said. “If you grow the market pie, you can aspire to have a bigger piece. If you are just focusing on the operating ratio, at some point, you might have a profitable pie, but you might not be participating in the full size of what the market can offer.”

Advertisement

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

If a railroad is hyper-focused on ensuring its locomotives leave the yard on time, or is willing to use the industry’s relative lack of competition to put shareholders ahead of customers, then the rest of us pay for it.

Goods producers are at the mercy of railways and their pinpoint calculations about how to keep their operating ratios low. That makes it harder for producers to get their merchandise to market. It also forces more stuff onto trucks, which clog the roads and increase carbon emissions. But at least shareholders are happy. CP’s stock price is about 40 per cent higher than it was a year ago, while CN’s shares have only increased about 14 per cent over the same period after falling about 10 per cent since announcing its intention in mid-April to bid for KCS.

KCS owns tracks that extend deep into Mexico, setting CN up to become the first truly North American railway. Its weaker share price suggests some investors are skeptical that regulators will allow that to happen. CN has promised to pay KCS US$1 billion if it fails to win approval, which likely won’t be known for at least a year.

“You need balance where you have low costs, but there comes a point in your low costs where you are no longer a railroad for your customer,” Ruest said. “Investors and analysts are more focused on the short term. We’re focused on the long term, and to be a relevant, long-term company, we need to focus on the people whose product we move, who pay the freight: our customers.”

Advertisement

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

A Canadian railroad that extends uninterrupted to the southernmost ports on the continent could mark the beginning of a new phase for the North American trading zone, which began with the original Canada-United States trade agreement, and later expanded to include Mexico in 1994.

Both Ruest and Creel said they made their bids for KCS because they sensed a change in the weather. Trade winds that have blown strongest across the Pacific Ocean for the past couple of decades are shifting, and both long-time shipping executives have said they anticipate a significant amount of factory production that had shifted to China will be “near-shored” in Mexico in the years ahead.

The new North American trade agreement appears to have quieted U.S. complaints about such an arrangement, removing political risk as a reason to proceed cautiously on making a big investment on north-south trade between Canada, the U.S. and Mexico. The attention of politicians in Washington has shifted to China, presenting companies that want to sell to Americans with an extra incentive to set up production inside the North American bloc.

Many of those companies would have been rethinking their supply chains anyway, because the pandemic exposed the risk of relying too heavily on low-cost factories located in only one part of the world.

This advertisement has not loaded yet, but your article continues below.

Article content

They also would have been assessing how to lower their carbon emissions, since consumers, investors and politicians have made it clear that operating a successful company now means being an active participant in the fight against climate change. That’s good for railways, because they can offer a greener alternative to trucks. Ruest talks about the trucking industry like he might a competing railway, pledging to do what he can to force thousands of the diesel-guzzling machines off the road if his acquisition of KCS is approved.

“We follow the economy,” he said. “We follow business where business is going next, and that’s why we’re calling this a growth story as opposed to a strictly operating-ratio story.”

India's economic growth likely picked up in the January-March quarter from the previous three months, but economists have grown more pessimistic about this quarter after a harsh second wave of COVID-19 hit the country last month.

The median forecast from a Reuters survey of 29 economists showed gross domestic product in Asia's third-largest economy grew 1.0% in the March quarter from a year earlier, up from 0.4% in the previous quarter when India began pulling out of a steep pandemic-induced recession in earlier six months. read more

But the second wave of infections and deaths across the world's second-hardest hit country has caused forecasters to trim their projections for the coming months.

The median forecast for April-June growth is 21.6%, down from a month-earlier estimate of 23% after the resurgence prompted most industrial states to impose lockdowns, throwing millions out of work. For the fiscal year to March 2022, economists cut their median forecast to 9.8% from 10.4%.

The statistics ministry is to announce the data at 1200 GMT.

India has recorded 27.9 million COVID-19 infections, behind only the United States, and 325,972 deaths as of Sunday, although the rise has begun to slow. read more

Prime Minister Narendra Modi's administration says the economic impact will not be as severe as last year, as lockdowns are looser this time and growth in manufacturing and exports is higher.

But Arun Singh, global chief economist at Dun & Bradstreet, said the downside risks to growth were intensifying as the second wave makes the return to pre-pandemic growth rates difficult.

"Owing to the intensifying nature of the pandemic and the spread to the rural areas, which were largely spared in 2020, we expect growth prospects to have deteriorated for 2021/22."

The central bank, which has kept monetary policy loose while boosting liquidity to the economy, said on Thursday that growth prospects will depend on how fast India can arrest infections. read more

Modi has faced criticism for the slow pace of his four-month-old vaccination campaign, which has inoculated fewer than 4% of India's 1.38 billion people. Analysts warn the slow rollout could pose medium-term risks to growth, especially if the country were to experience a third wave of COVID-19.

The economy, which was facing a slowdown even before the pandemic, now confronts a crash of consumer demand - constituting over 55% of the economy - as household incomes and jobs have declined.

Unemployment soared to a near one-year high of 14.73% in the week ending May 23, according to the Centre for Monitoring Indian Economy, a Mumbai-based private think tank.

Finance Minister Nirmala Sitharaman, who said on Friday that no decision has been taken for another stimulus package, has limited space due to a fall in tax collections and rising public debt.

(Bloomberg) -- Turkey’s economy has continued to grow at a strong pace so far this year, but that doesn’t necessarily mean its citizens are getting richer.

The $717 billion economy likely outperformed all Group of 20 nations except for China in the first quarter after nearly stalling a year ago when the pandemic struck. It’s been bolstered by robust consumption on the back of last year’s government-led credit push, an expansion that came at the expense of price and currency stability.

Data on Monday is likely to show gross domestic product rose 6.3% from a year earlier and 1.3% from the fourth quarter, according to the medians of forecasts in Bloomberg surveys. Treasury and Finance Minister Lutfi Elvan said Thursday that “data point to 6% growth in the first quarter.”

There is an “exchange rate illusion” in Turkey’s economic growth data, according to Enver Erkan, chief economist at Istanbul-based Tera Yatirim, who’s ranked by Bloomberg as the most accurate forecaster on Turkish GDP data.

Noting that the GDP per capita in U.S. dollar terms dropped nearly 40% since 2013 to around $7,700 last year, Erkan said Turkey’s recent economic model isn’t sustainable as the growth is mainly driven by consumption supported by government spending and loan campaigns.

“This comes at the expense of lira and price stability,” he said.

The government pushed banks to ramp up lending to help businesses and consumers ride out last year’s Covid-19 emergency. The credit boom was coupled with a front-loaded easing cycle that helped prime the economy. That growth push weakened the currency by 20% last year and kept headline inflation in double digits. The size of the economy dropped to $717 billion last year from $760.8 billion a year earlier.

The currency further lost 10% against the dollar in the first quarter, especially after President Recep Tayyip Erdogan fired the central bank’s former hawkish governor Naci Agbal in March. The decision to fire Agbal, who had sought to restore the central bank’s credibility, set off a swift reversal of investor enthusiasm, sending Turkish markets into a nosedive.

The data expose the challenge facing new central bank Governor Sahap Kavcioglu as he looks to restore price stability without cooling the economy ahead of the general elections in 2023.

Kavcioglu has pledged policy continuity after his appointment and kept benchmark interest rate unchanged at 19% for a second meeting this month, saying the pace of price gains had peaked in April. Consumer inflation quickened for a seventh month to 17.14% in April.

NEW DELHI — India’s economic growth likely picked up in the January-March quarter from the previous three months, but economists have grown more pessimistic about this quarter after a harsh second wave of COVID-19 hit the country last month.

The median forecast from a Reuters survey of 29 economists showed gross domestic product in Asia’s third-largest economy grew 1.0% in the March quarter from a year earlier, up from 0.4% in the previous quarter when India began pulling out of a steep pandemic-induced recession in earlier six months.

But the second wave of infections and deaths across the world’s second-hardest hit country has caused forecasters to trim their projections for the coming months.

The median forecast for April-June growth is 21.6%, down from a month-earlier estimate of 23% after the resurgence prompted most industrial states to impose lockdowns, throwing millions out of work. For the fiscal year to March 2022, economists cut their median forecast to 9.8% from 10.4%.

The statistics ministry is to announce the data at 1200 GMT.

India has recorded 27.9 million COVID-19 infections, behind only the United States, and 325,972 deaths as of Sunday, although the rise has begun to slow.

Article content

Prime Minister Narendra Modi’s administration says the economic impact will not be as severe as last year, as lockdowns are looser this time and growth in manufacturing and exports is higher.

But Arun Singh, global chief economist at Dun & Bradstreet, said the downside risks to growth were intensifying as the second wave makes the return to pre-pandemic growth rates difficult.

“Owing to the intensifying nature of the pandemic and the spread to the rural areas, which were largely spared in 2020, we expect growth prospects to have deteriorated for 2021/22.”

The central bank, which has kept monetary policy loose while boosting liquidity to the economy, said on Thursday that growth prospects will depend on how fast India can arrest infections.

Modi has faced criticism for the slow pace of his four-month-old vaccination campaign, which has inoculated fewer than 4% of India’s 1.38 billion people. Analysts warn the slow rollout could pose medium-term risks to growth, especially if the country were to experience a third wave of COVID-19.

The economy, which was facing a slowdown even before the pandemic, now confronts a crash of consumer demand – constituting over 55% of the economy – as household incomes and jobs have declined.

Unemployment soared to a near one-year high of 14.73% in the week ending May 23, according to the Centre for Monitoring Indian Economy, a Mumbai-based private think tank.

Finance Minister Nirmala Sitharaman, who said on Friday that no decision has been taken for another stimulus package, has limited space due to a fall in tax collections and rising public debt. (Reporting by Manoj Kumar; Editing by William Mallard)

Forecasts suggest GDP could drop by up to 12%; it dropped 5.1% and 89% of lost jobs gave been restored

Author of the article:

Gordon Hoekstra

Publishing date:

May 30, 2021 • 2 hours ago • 3 minute read

A sign of the times in January. The economy has been affected unevenly by the pandemic and there is a possibility of more business failures even as pandemic restriction go away.Photo by Jason Payne /PNG

Article content

B.C.’s economy has weathered the COVID-19 pandemic better than expected, economists say, but there may still be pain to come as government support programs end.

In the early days of the pandemic, in March, 2020, the Business Council of B.C. forecast an unprecedented seven to 12 per cent drop in gross domestic product, a measure of the total value of the economy.

But recently, the B.C.-government appointed economic forecast council estimated the province’s GDP had declined 5.1 per cent in 2020. A recent Statistics Canada estimate pegged the decrease at about four per cent.

Economists agree the pandemic’s effect has not been even across the economy. Those in construction, export and resource industries, and in service and technology sectors that could work at home have fared better than those, for example, working in restaurants, pubs and hotels.

The B.C. government’s restart plan announced last week sets out steps for reopening some of those hard-hit areas, including lifting provincial travel restrictions on June 15 and allowing casinos and nightclubs to reopen on July 1. Larger gatherings such as concerts may be allowed by Sept. 1.

Advertisement

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

The eased restrictions are tied to increased vaccinations of British Columbians, with nearly 70 per cent of adults in the province already having at least one dose.

“I would say the B.C. economy is in pretty good shape. It’s pretty healthy,” said Ken Peacock, chief economist and senior vice-president at the Business Council of British Columbia.

Peacock said the business council’s more severe forecast didn’t materialize because B.C.’s lockdown in the spring of 2020 didn’t last as long as expected, massive government spending has supported businesses and individuals, and many businesses have adapted better than anticipated.

Harder-hit sectors like food services, accommodation and culture and entertainment will be helped by the phased restart plan, he said.

International travel remains more of a question mark, although a reopening of the U.S. border with Canada, expected sometime this year, will also be a boost, he said.

Jeremy Stone, the director of Simon Fraser University’s community economic development program, says a concern as restrictions ease is whether businesses that have used up savings or borrowed money will be able to survive.

That will be clearer when government support programs are eliminated, said Stone, who helped co-manage a $20-million grant and loan program following Hurricane Katrina that devastated New Orleans in 2005.

Stone said he expects some businesses will continue to go under even as restrictions are lifted.

Advertisement

Story continues below

This advertisement has not loaded yet, but your article continues below.

Article content

Businesses may have put so much money into staying afloat during the pandemic they don’t have the capital to deal with day-to-day problems such as a refrigerator breaking down, noted Stone.

And retailers may have to deal with changed buying habits of people, such as buying online or a change of priorities, where spending does not go into consumer goods such as a diamond ring, he said.

“I think this is a very tenuous time … the next six months to a year for all businesses, regardless of whether or not we’re fully reopened,” said Stone.

Bryan Yu, Central 1 Credit Union’s chief economist, said the economy has performed better than expected.

A recent forecast by Credit 1 has the province’s economy growing 4.2 per cent this year and by 4.5 per cent in 2022 before slowing to below three per cent in 2023.

Forecast seven per cent growth in the U.S. economy will also help, said Yu.

He noted that B.C. has already regained 89 per cent of jobs lost during the initial stages of the pandemic, but tourism-related employment remains sharply below pre-pandemic levels.

The restart will help the harder-hit sectors, said Yu.

“That’s as long as we can maintain this trend of lower COVID cases as well as the hope we won’t see some spike in new variants that could kind of derail this process,” he said.

/cloudfront-us-east-2.images.arcpublishing.com/reuters/IQ6F7KVDRZLPRPX432XF75WMPI.jpg)